- GRIT

- Posts

- 👉 5 of the Mag 7 Report Earnings This Week!

In partnership with

Welcome to your new week.

During market swings, it’s always best to stay well-informed! If you want full access to our Week in Review editions, monthly livestreams , portfolio access, monthly stock deep dives, and more — consider upgrading your subscription.

Let’s dive right in.

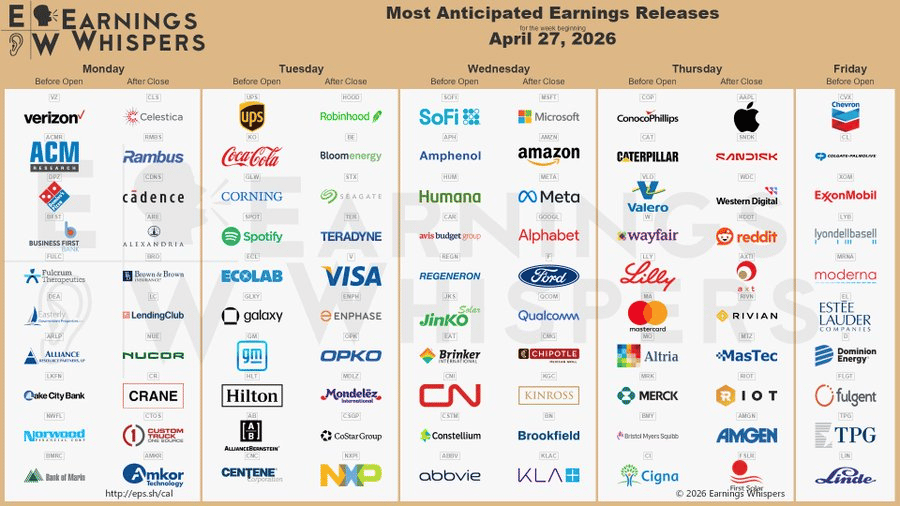

Key Earnings Announcements:

It’s a huge one… 5 of the Mag 7 report this week.

Monday (4/27): Verizon, Nucor, Cadence, Rambus, Celestica, Alexandria Real Estate, LendingClub

Tuesday (4/28): UPS, Coca-Cola, Spotify, Visa, Corning, General Motors, Hilton, Ecolab, Mondelez

Wednesday (4/29): Microsoft, Meta Platforms, Alphabet, Amazon, Qualcomm, Ford, Chipotle, Regeneron, Brookfield

Thursday (4/30): Apple, Eli Lilly, Mastercard, Merck, Amgen, Reddit, Western Digital, Caterpillar, McDonald’s

Friday (5/1): ExxonMobil, Chevron, Moderna, Linde, Estée Lauder, Dominion Energy, TPG

What We’re Watching:

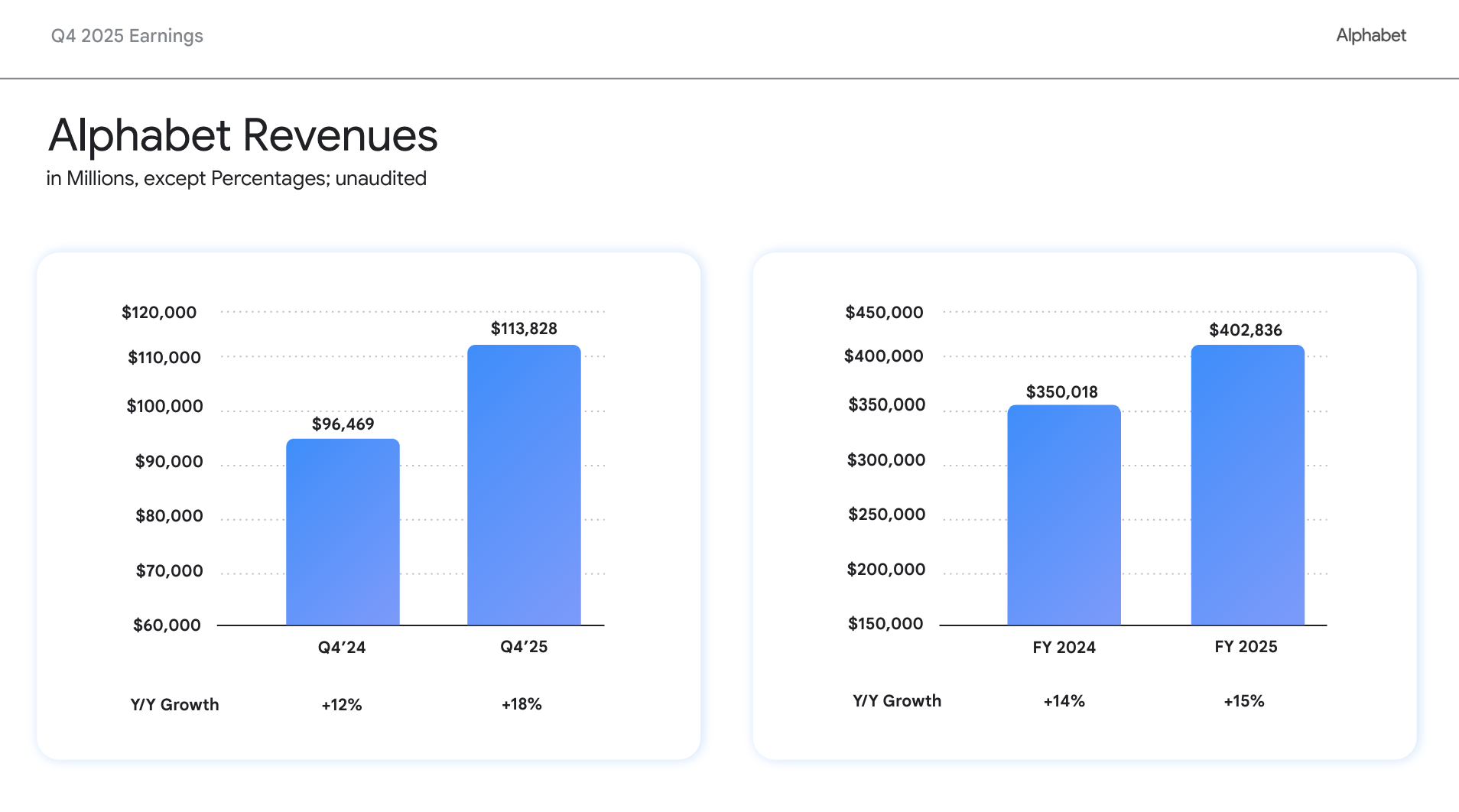

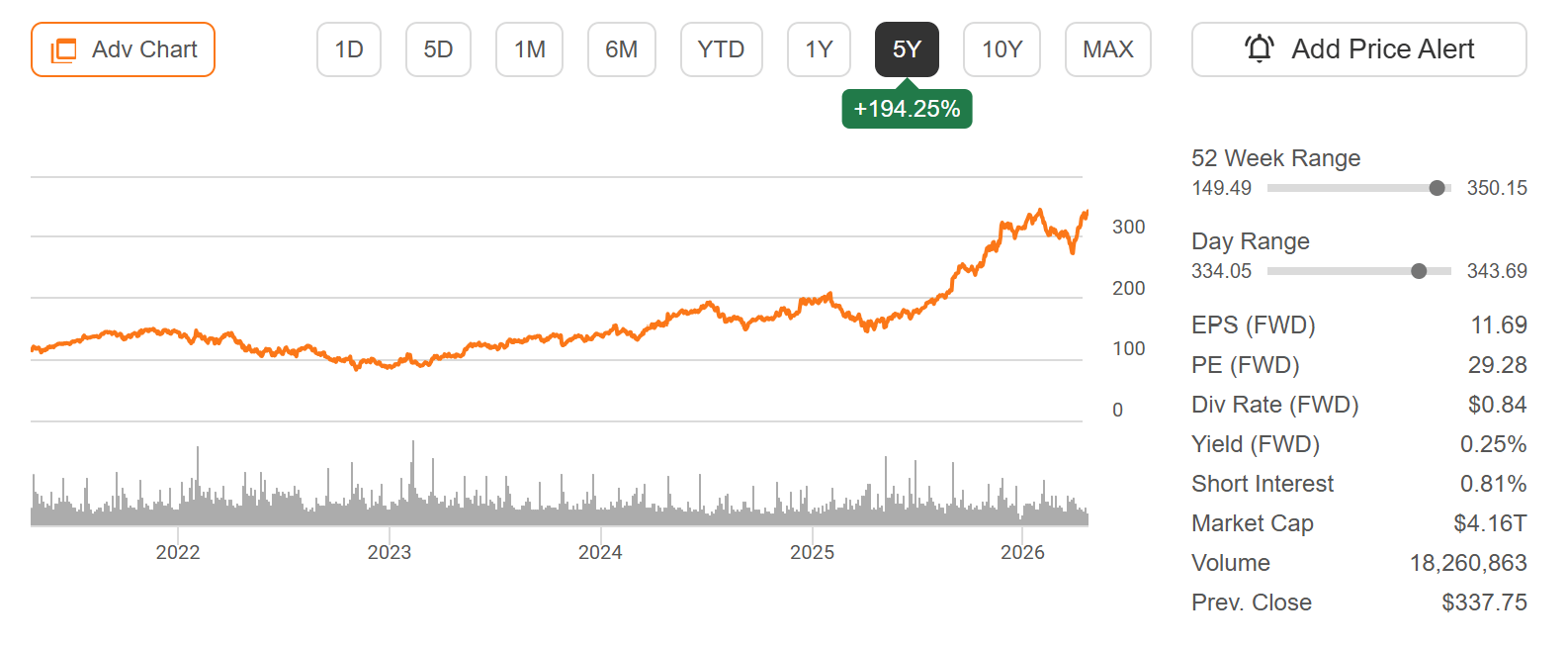

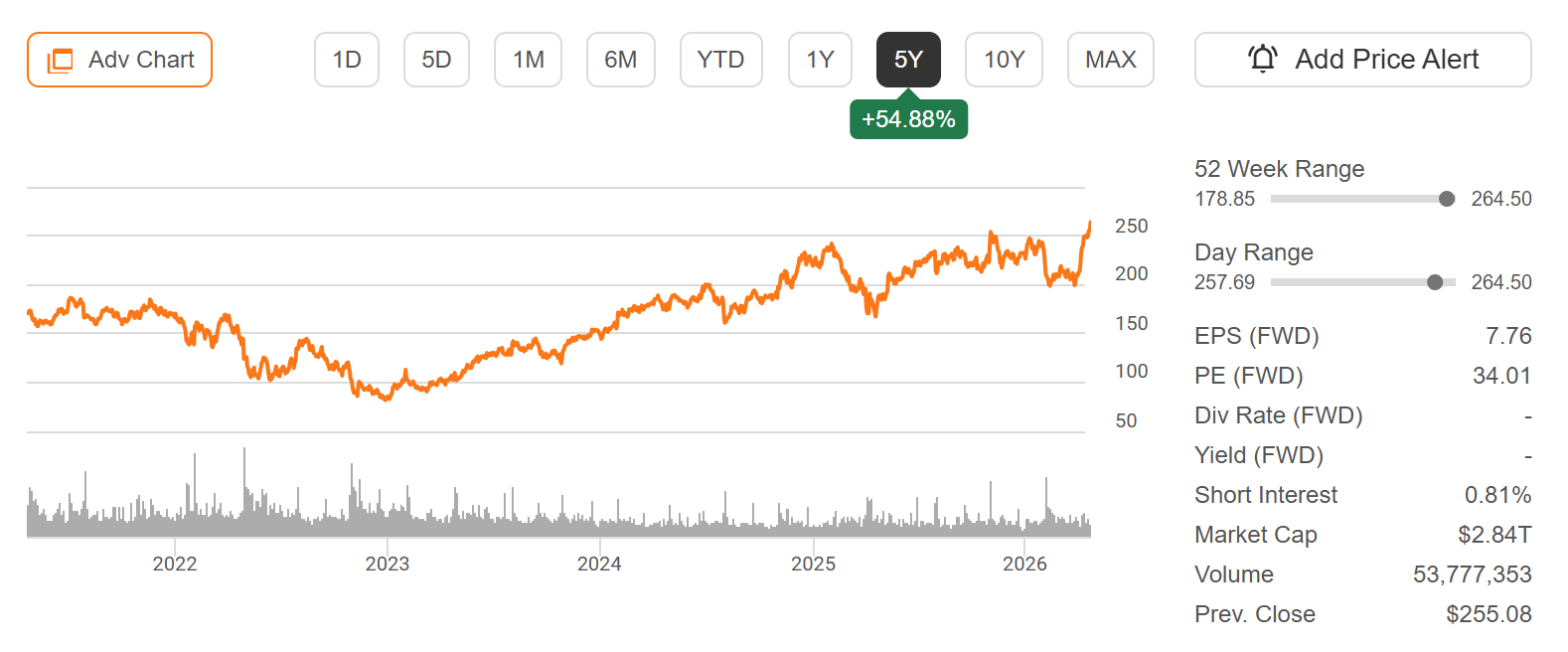

Alphabet (GOOG)

Alphabet (+9% YTD) reports this week with shares hovering near highs, as investors look for confirmation that AI-driven momentum can continue to support both growth and margins.

Google search and cloud are in the spotlight. Search has held up better than many expected despite rising competition from generative AI platforms, while YouTube continues to benefit from improving ad spend and strong engagement. Meanwhile, Google Cloud has been a bright spot, with accelerating growth and expanding margins driven by enterprise AI demand and cost discipline.

The key debate now centers on monetization vs. cost. Alphabet is aggressively investing in AI infrastructure, custom chips (TPUs), and model development to compete with peers, but those investments are pressuring margins in the near term. At the same time, the company is rolling out AI features across Search, Workspace, and Cloud, aiming to turn usage into incremental revenue over time.

Heading into this print, I’ll be watching: search ad trends, Cloud growth and margins, AI monetization signals, and any updates on capex intensity tied to AI infrastructure. Commentary on competition and user behavior shifts in search will also be critical.

“We are investing responsibly in AI to support long-term growth across our products and services.”

Alphabet, Inc. (GOOG) Stock Performance, 5-Year Chart, Seeking Alpha

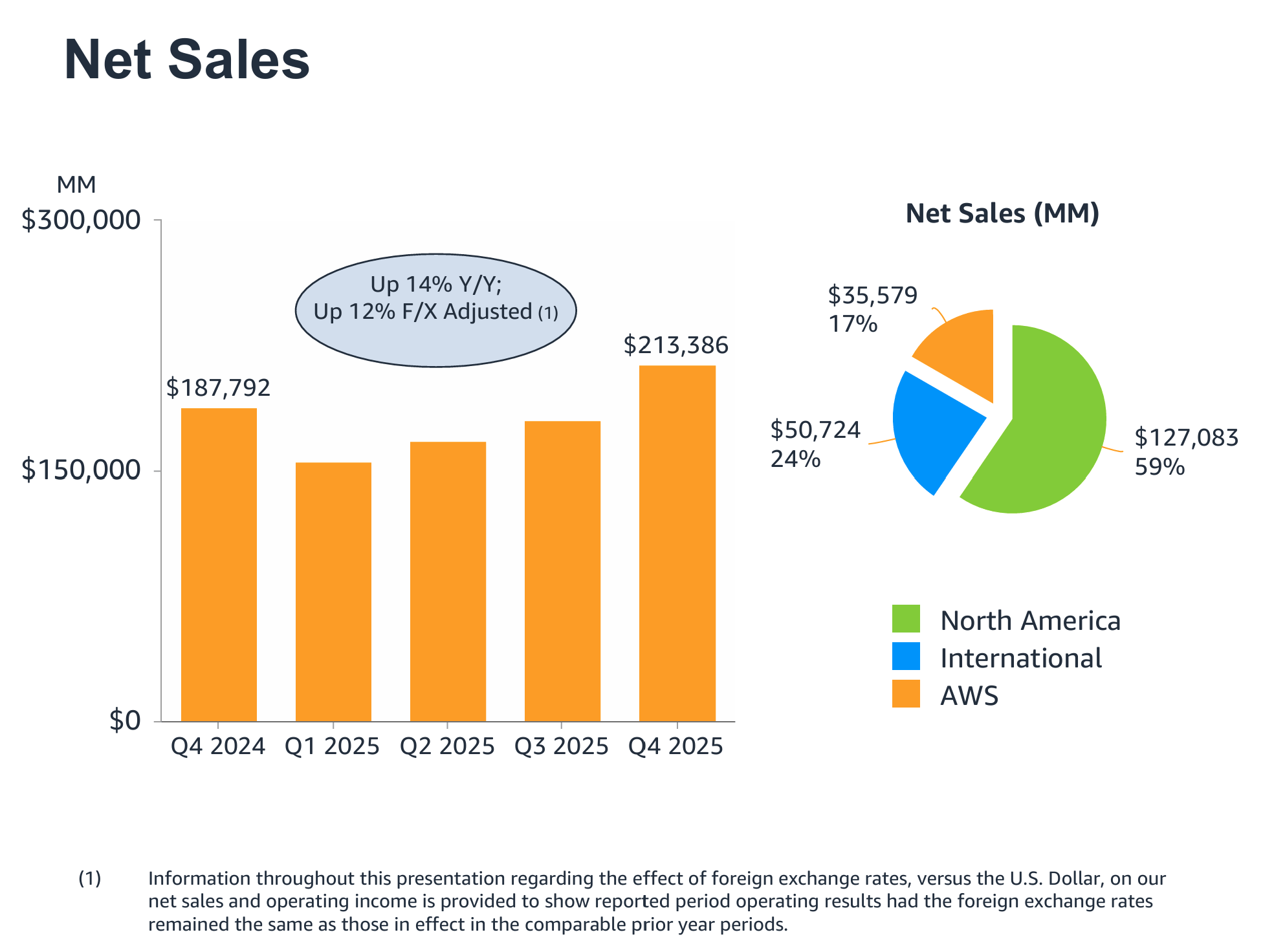

Amazon (AMZN)

Amazon (+14.3% YTD) reports this week with the focus squarely on whether accelerating AWS growth can justify the company’s massive AI-driven spending cycle.

The core story remains AWS and advertising. AWS has reaccelerated, posting ~24% growth last quarter — its fastest pace in over a year — driven by surging demand for AI infrastructure and enterprise workloads. At the same time, Amazon’s high-margin advertising business continues to scale rapidly, benefiting from Prime Video, retail traffic, and improved ad targeting.

Amazon is guiding for an unprecedented ~$200B in capex this year, largely tied to AI infrastructure, data centers, and custom silicon. While management frames this as necessary to meet demand and extend AWS leadership, investors remain cautious about near-term margin pressure and return timelines.

Last quarter, Amazon delivered strong top-line growth and expanding operating income, with AWS continuing to drive the majority of profitability despite representing a smaller share of total revenue.

Heading into this print, I’ll be watching: AWS growth trajectory, capex outlook, AI monetization signals, and margin durability across both cloud and retail. Any commentary around demand visibility and ROI on AI investments will be critical for the stock’s next move.

“We’re investing aggressively to meet what we believe is a once-in-a-generation opportunity in AI.”

Amazon, Inc. (AMZN) Stock Performance, 5-Year Chart, Seeking Alpha

Rex Gelb spent a decade building HubSpot's paid engine. Now he's showing founders exactly how to do it.

On April 27th, get the framework to structure, launch, and scale paid media that drives pipeline, not just traffic. 20 minutes. Live Q&A. Free.

Investor Events / Global Affairs:

Market remains on Iran watch and Pershing Square prices its IPO.

Iran Watch

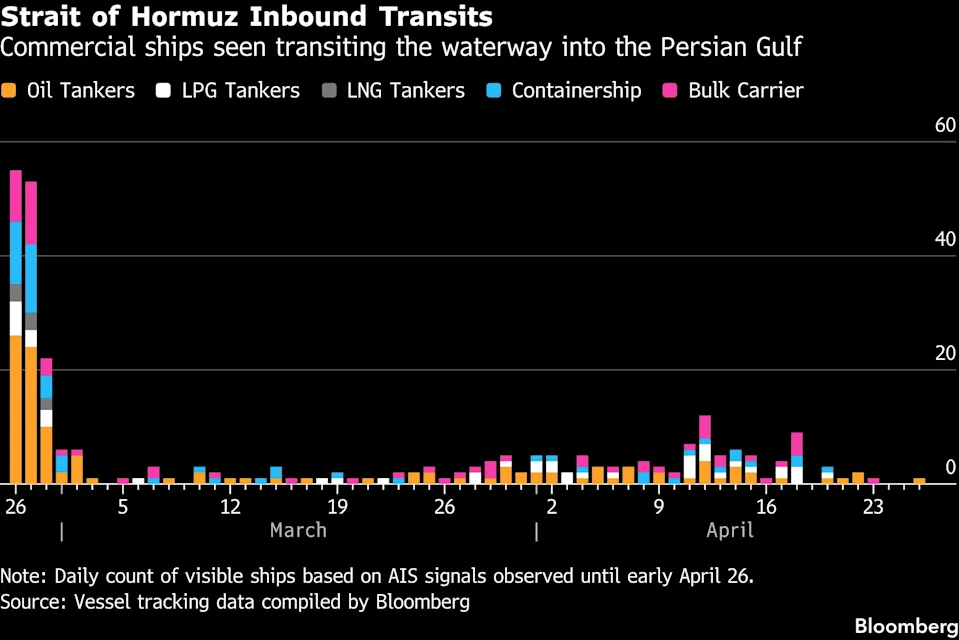

Markets will enter the week on high alert as rapidly evolving developments in the Middle East continue to drive volatility across energy, equities, and global risk sentiment.

Over the weekend, Donald Trump signaled a shift in diplomatic strategy, stating the U.S. will not send envoys to Pakistan for in-person talks with Iran, instead suggesting negotiations could take place remotely — a move that underscores the fragile and uncertain state of diplomacy.

At the same time, tensions in key shipping lanes escalated further after Iran’s Islamic Revolutionary Guard Corps (IRGC) reportedly boarded commercial vessels near the Strait of Hormuz, while officials indicated efforts to establish a “new maritime regime” in the region. Additional pressure points include U.S. naval interceptions in the Arabian Sea and continued Israeli military activity in Lebanon.

The situation remains highly fluid, with limited clarity on whether diplomatic progress will materialize or further escalation will occur. For markets, the implications are immediate — particularly for oil supply, shipping routes, and inflation expectations, all of which have shown heightened sensitivity to weekend headlines.

"These are sensitive diplomatic discussions and the U.S. will not negotiate through the press. As the president has said, the United States holds the cards and will only make a deal that puts the American people first, never allowing Iran to have a nuclear weapon.”

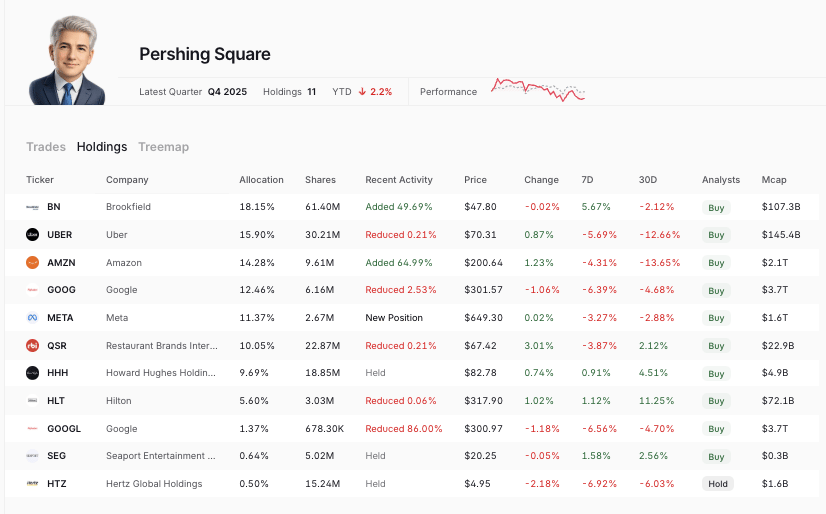

Pershing Square IPO

Pershing Square USA (PSUS) is expected to price its IPO and begin trading this week, offering public market investors direct exposure to the investment strategy of Bill Ackman.

The structure is notable — investors will gain access not only to Pershing Square’s concentrated equity portfolio, but also a small economic stake in the underlying management company, creating a hybrid between a traditional investment fund and an asset manager.

The deal comes at a time when interest in active management and “star investor” vehicles is resurging, particularly as market volatility and macro uncertainty create a more favorable backdrop for differentiated strategies.

For investors, the key questions will center around valuation, fee structure, and how the vehicle trades relative to its underlying net asset value (NAV) — a dynamic that has historically driven performance in similar publicly traded funds.

“The dual structure gives investors the chance to trade the fund just like they would a stock, benefit from the portfolio appreciation, and also gain from the fees generated by the fund through exposure to Pershing Square Inc. This hybrid return profile is almost a signature move from Bill Ackman, who is known for his innovation and outrageous bets. Ackman launched Pershing Square Tontine Holdings (PSTH) back in 2020 and marketed it as an improvement on special purpose acquisition companies (SPACs), but failed to close any deal.”

Major Economic Events:

FOMC interest rate decision and the Fed's preferred inflation gauge – PCE

Monday (4/27): N/A

Tuesday (4/28): Consumer confidence, S&P Case-Shiller home price index

Wednesday (4/29):Building permits, Durable goods orders, FOMC rate decision, Housing starts

Thursday (4/30): Chicago PMI, Core PCE, Employment cost index, GDP, Initial jobless claims, PCE index, Personal income, Personal spending

Friday (5/1): ISM manufacturing, S&P manufacturing PMI

What We’re Watching:

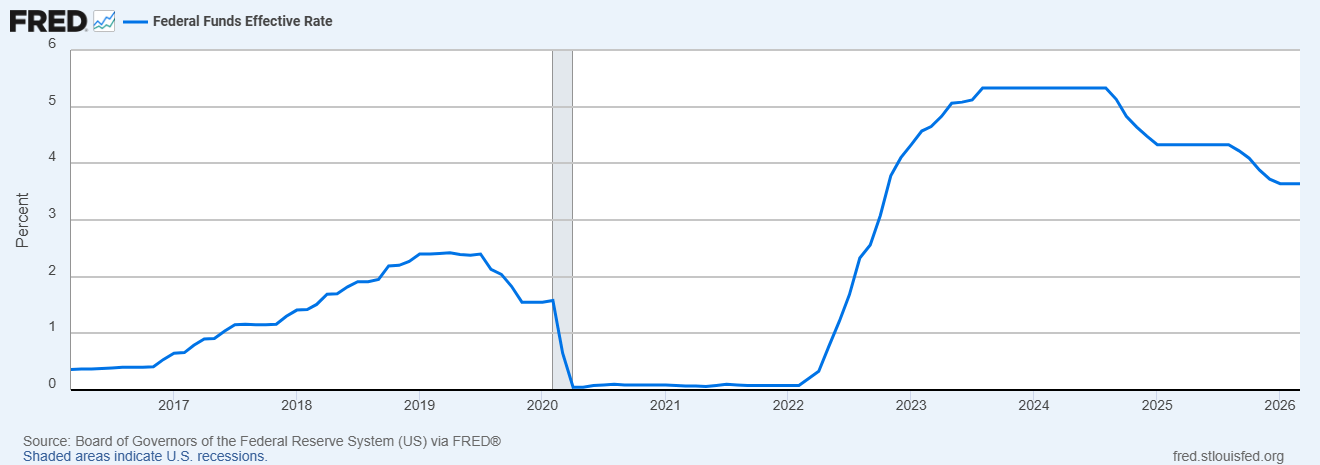

Fed Interest Rate Decision

The Federal Reserve left the federal funds rate unchanged at 3.50%–3.75% for a second consecutive meeting in March, in line with expectations, as policymakers continue to navigate a more uncertain inflation outlook.

Minutes from the meeting revealed a more two-sided policy debate, with some officials noting that rate hikes could still be warranted if inflation proves persistent, while others remain open to eventual cuts if price pressures ease. The vast majority of participants flagged elevated upside risks to inflation and downside risks to employment, both of which have intensified amid recent geopolitical developments.

A key concern is the impact of the Middle East conflict, where higher energy prices could feed through into broader inflation and delay progress toward the Fed’s target. Despite holding rates steady, policymakers still signaled one rate cut in 2026 and another in 2027, though the timing remains highly data-dependent.

Economists expect the following this week:

Fed Funds Rate: 3.50%–3.75% vs. unchanged prior

Policy Outlook: Bias toward eventual cuts, but rising inflation risk

“The possibility of stagflation outbreak coming from high oil prices before the tariff inflation went away, leading to the main engine of growth – the U.S. consumer – just giving up and saying we don't have confidence, we're going to start hoarding our money, and sending us into a stagflationary recession – that'd be the worst outcome.”

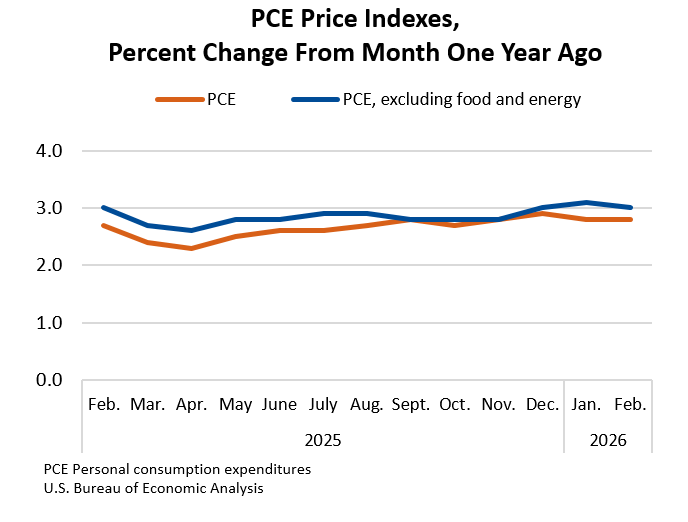

Personal Consumption Expenditures

The Core PCE Price Index – the Federal Reserve’s preferred measure of inflation – rose 0.4% MoM in February, matching expectations and marking a third consecutive month at a 10-month high, signaling that underlying price pressures remain sticky.

On an annual basis, core PCE increased 3.0% YoY, easing slightly from 3.1% in January but still well above the Fed’s 2% target, reinforcing the narrative that inflation progress has slowed.

The persistence in monthly gains is the key concern for policymakers. Even as year-over-year readings gradually trend lower, elevated monthly prints suggest inflation may be stabilizing above target rather than continuing a smooth decline.

Economists expect the following this week:

Core PCE (MoM): +0.4% vs. +0.4% prior

Core PCE (YoY): 3.0% vs. 3.1% prior

“What I’m most interested in is: What’s the underlying inflation rate? Not: What’s the one-time change in prices because of a change in geopolitics or change in beef? The measures I prefer are looking at things that are called trimmed averages. We take out all of the tail-risks, all of the one-off items, and we ask ourselves whether the generalized change in prices is having second-order effects on the economy.”

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

This content is sponsored by NEOS Investments. The creator is compensated by NEOS to discuss NEOS ETFs. This content is for informational purposes only, and is not personalized investment, tax, or legal advice, and does not constitute an offer to buy or sell any security. Investing involves risk, including possible loss of principal. Before investing, carefully review the NEOS ETFs prospectus at neosfunds.com.

Grit is a publisher of financial information, not an investment advisor. Grit does not provide personalized or individualized investment advice or information that is tailored to the needs of any particular recipient. Grit does not guarantee the accuracy or completeness of the information provided in this page. All statements and expressions herein are the sole opinion of the author or paid advertiser.

Cover Image Source: Microsoft UK Stories

THE INFORMATION CONTAINED ON THIS WEBSITE IS NOT AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE, AND DOES NOT PURPORT TO BE AND DOES NOT EXPRESS ANY OPINION AS TO THE PRICE AT WHICH THE SECURITIES OF ANY COMPANY MAY TRADE AT ANY TIME. THE INFORMATION AND OPINIONS PROVIDED HEREIN SHOULD NOT BE TAKEN AS SPECIFIC ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. INVESTORS SHOULD MAKE THEIR OWN INVESTIGATION AND DECISIONS REGARDING THE PROSPECTS OF ANY COMPANY DISCUSSED HEREIN BASED ON SUCH INVESTORS’ OWN REVIEW OF PUBLICLY AVAILABLE INFORMATION AND SHOULD NOT RELY ON THE INFORMATION CONTAINED HEREIN. INVESTORS SHOULD OBTAIN INDIVIDUAL INVESTMENT ADVICE BASED ON THEIR OWN CIRCUMSTANCES BEFORE MAKING AN INVESTMENT DECISION

No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned.

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Any projections, market outlooks or estimates herein are forward looking statements and are inherently unreliable. They are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities discussed herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and Grit undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional material.

Grit does not accept any liability whatsoever for any direct or consequential loss, however arising, directly or indirectly, from any use of the information contained herein.

By using the Site or any related social media account, you are indicating your consent and agreement to this disclaimer and our terms of use. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Please read: Terms of Use, Privacy Policy, Disclosure Policy and Disclaimer Policy

If you have any questions please contact us at [email protected]