- GRIT

- Posts

- 👉 A Volatile Week Ahead?

Welcome to your new week.

The Iran conflict will be the primary focus of the week, paired with some massive earnings reports + investor events.

Read on for everything you need to watch over the coming days.

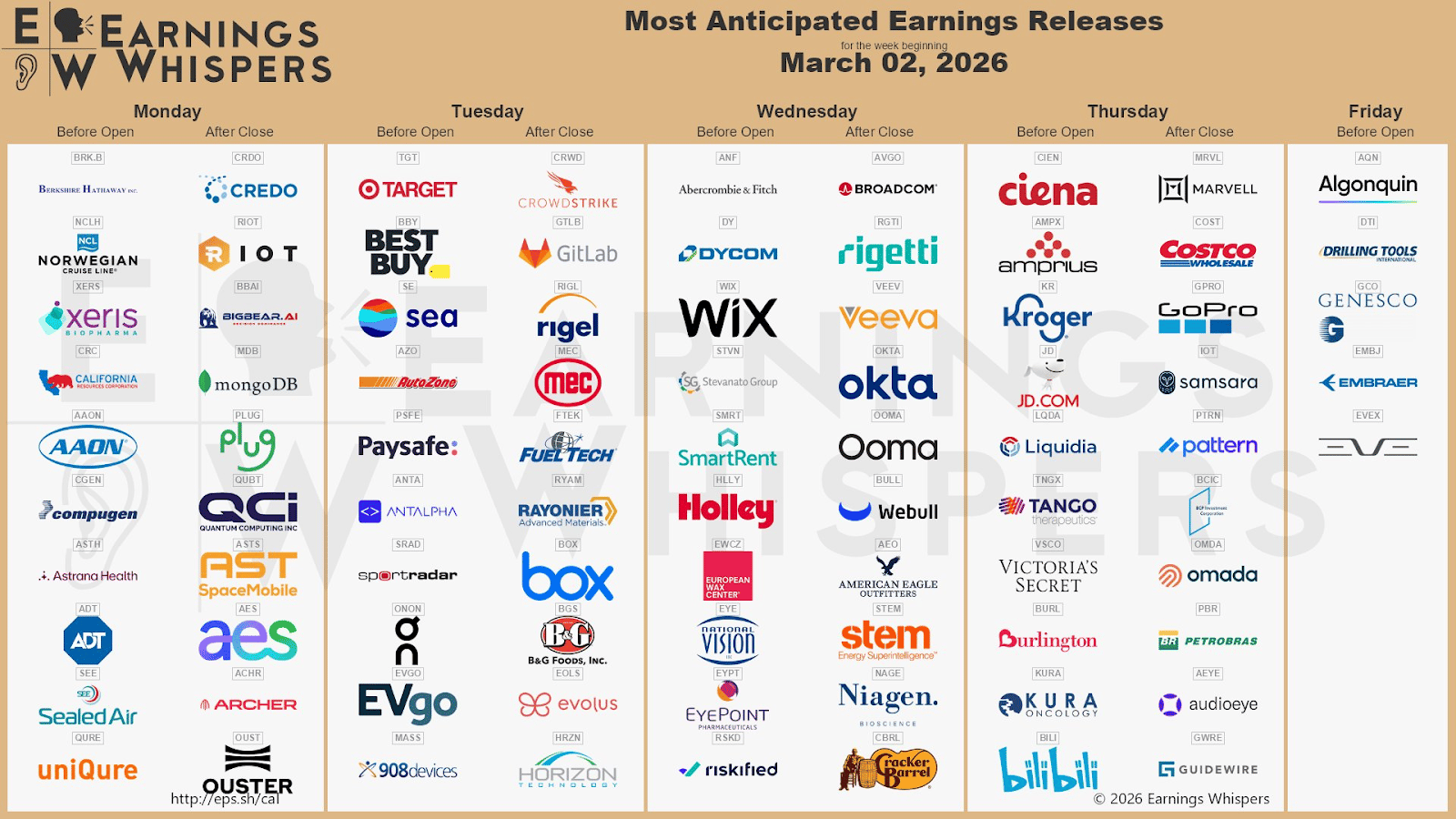

Key Earnings Announcements:

Abercrombie and Fitch, Broadcom, CrowdStrike, Marvell, and Target highlight this week.

Monday (3/2): Credo Technology, MongoDB, Norwegian Cruise Line, Riot Platforms, Sealed Air

Tuesday (3/3): Best Buy, CrowdStrike, GitLab, On Holding, Sportradar, Target

Wednesday (3/4): Abercrombie & Fitch, Broadcom, Okta, Rigetti Computing, Veeva Systems, Wix

Thursday (3/5): Costco, Kroger, Marvell Technology, Samsara, Victoria’s Secret, Burlington Stores

Friday (3/6): Embraer, Genesco, Petrobras

What We’re Watching:

Broadcom (AVGO)

Source: Broadcom Investor Relations

Broadcom (-7.% YTD) reports Q1 FY2026 earnings Wednesday after the close, with investors focused on whether the company can continue translating massive AI-infrastructure demand into sustained revenue growth – and justify its position as one of the market’s most important AI enablers outside of Nvidia.

Broadcom has emerged as a critical backbone of the AI buildout through its custom accelerators, networking silicon, and VMware-driven infrastructure software platform, supplying hyperscalers building next-generation data centers. Management previously guided Q1 revenue to roughly $19.1 billion, supported by expectations that AI semiconductor revenue will double year-over-year to about $8.2 billion, driven by strong orders from large cloud customers.

Last year, Broadcom generated $64 billion in total revenue (+24% YoY), with AI-related sales surging 65% to ~$20 billion, increasingly becoming the primary engine of growth as enterprise customers scale AI workloads.

Heading into this release, I’ll be watching whether AI demand continues accelerating beyond GPU spending into networking and custom silicon, how VMware integration is impacting margins and recurring software revenue, and whether management provides updated visibility on its growing AI backlog – now viewed as one of the clearest multi-year demand signals across semiconductor infrastructure.

“We expect AI revenue to continue to accelerate and drive most of our growth.”

Broadcom Inc. (AVGO) Stock Performance, 5-Year Chart, Seeking Alpha

Target (TGT)

Source: Target Investor Relations

Target Corporation (+16.4% YTD) reports Q4 FY2025 earnings Tuesday before the open. The company enters this release at an important inflection point for big-box retail. While holiday shopping trends improved late in the quarter, elevated promotions, inventory normalization efforts, and ongoing shifts toward essentials over discretionary categories continue to weigh on profitability. Management has already indicated results are expected to land broadly in line with prior guidance, signaling limited upside surprises heading into the print.

Last quarter, Target delivered mixed results as comparable sales remained pressured despite steady traffic trends, with margins constrained by markdown activity and category mix. Analysts currently expect roughly $30B+ in quarterly revenue and EPS near ~$2.15, as investors look for signs that earnings can reaccelerate into FY2026 following a weaker FY2025 performance.

Heading into earnings, I’ll be watching three key themes: holiday-season execution, progress in discretionary categories like home and apparel, and commentary on pricing power amid still-selective consumer behavior. Updates on inventory discipline, private-label momentum, and digital fulfillment profitability will likely drive sentiment for the stock’s next move.

“Our team is focused on delivering value, managing inventory carefully, and returning to sustainable, profitable growth.”

Target Corp (TGT) Stock Performance, 5-Year Chart, Seeking Alpha

Investor Events / Global Affairs:

Apple Experience + new product announcements, Morgan Stanley TMT Conference, Continued focus on Iran.

Apple Experience

Apple Inc. has invited press, developers, and creators to in-person “Apple Experience” sessions across New York, London, and Shanghai, coinciding with coordinated announcements tied to its latest iPad and Mac product refresh cycle.

The events are expected to provide hands-on demonstrations of new hardware and software integrations, with markets watching closely for updates around AI-enabled productivity features, silicon performance upgrades, and ecosystem expansion across devices.

In addition, new products are most likely to be revealed this week. A MacBook Air with an M5 chip, MacBook Pros with M5 Pro and M5 Max chips, a lower-cost MacBook featuring the A18 Pro chip, the iPad 12 with an A19 chip, an iPad Air with the M4 chip, and the iPhone 17e featuring the A19 chip, are expected according to various reports.

Apple Inc. (AAPL) Stock Performance, 5-Year Chart, Seeking Alpha

“Innovation at Apple has always been about bringing powerful technology into the hands of users in intuitive ways.”

Morgan Stanley TMT Conference Kicks Off in San Francisco

The annual Morgan Stanley Technology, Media & Telecom Conference begins this week in San Francisco, bringing together senior executives, institutional investors, and analysts for three days of strategy updates and industry outlook discussions across technology, media, and communications.

Notable presenters include Walmart Inc., Cisco Systems, The Walt Disney Company, Comcast Corporation, Expedia Group, Autodesk, NetApp, and Carvana, among others.

Morgan Stanley (MS) Stock Performance, 5-Year Chart, Seeking Alpha

Markets will be watching for commentary on enterprise IT spending, advertising trends, cloud demand, consumer health, and AI monetization, as management teams provide updated views ahead of the next earnings cycle.

Continued Focus on Conflict w/ Iran

Source: White House | Via AFP-JIJI

The U.S.–Israel conflict with Iran has entered its third day following coordinated strikes that killed Supreme Leader Ayatollah Ali Khamenei, triggering widespread retaliation across the region. Iran has launched missiles and drones at Israel and Gulf nations hosting U.S. bases, with civilian infrastructure in places like Dubai also hit. Casualties are mounting on both sides, and a temporary leadership council has assumed control in Tehran as succession questions loom.

Markets reacted swiftly. Oil surged roughly 8–9% on fears of supply disruptions, while gold and silver climbed as investors rotated into safe-haven assets. U.S. equity futures fell about 1%, and Asian markets opened lower, reflecting broader risk-off sentiment. The dollar firmed slightly, and Treasury yields remain volatile.

The big question now is whether tensions de-escalate or spiral. President Trump suggested the conflict could last weeks but also hinted at potential talks, while Iranian officials publicly rejected negotiations. Global reactions remain divided, with Western allies largely backing the U.S. and China and Russia condemning the strikes. For investors, the path of energy prices and the risk of regional spillover will likely dictate near-term market direction.

“They want to talk, and I have agreed to talk, so I will be talking to them. They should have done it sooner. They should have given what was very practical and easy to do sooner. They waited too long.”

Major Economic Events:

Jobs report, retail sales and a look into manufacturing highlight the week.

Monday (3/2): Auto Sales, ISM Manufacturing, S&P Final U.S. Manufacturing PMI

Tuesday (3/3): Kansas City Fed President Jeff Schmid Speaks, Minneapolis Fed President Neel Kashkari Interview, New York Fed President John Williams Remarks

Wednesday (3/4): ADP Employment, Fed Beige Book, ISM Services, S&P Final U.S. Services PMI

Thursday (3/5): Chicago Fed President Austan Goolsbee Speaks, Fed Vice Chair for Supervision Michelle Bowman Speaks, Import Price Index, Import Price Index ex-Fuel, Initial Jobless Claims, U.S. Productivity

Friday (3/6): Cleveland Fed President Beth Hammack Speaks, San Francisco Fed President Mary Daly Speaks, U.S. Employment Report, U.S. Hourly Wages, U.S. Unemployment Rate, Wage Growth (YoY)

What We’re Watching:

U.S. Retail Sales

U.S. retail sales were unchanged in December, missing expectations for a +0.4% increase and marking a sharp slowdown after November’s strong +0.6% gain. The report suggests holiday spending momentum cooled late in the year as higher borrowing costs and stretched household budgets continued to weigh on discretionary demand.

Strength in building materials (+1.2%), sporting goods (+0.4%), and gasoline stations (+0.3%) was offset by declines across several consumer-sensitive categories, including furniture (-0.9%), clothing (-0.7%), electronics (-0.4%), and auto dealers (-0.2%).

Importantly, control-group sales – the component used to calculate GDP – fell 0.1%, the first decline in three months, signaling softer underlying consumption entering 2026.

Economists expect the following this week:

Retail Sales (MoM): 0.0% vs. +0.6% prior

Retail Sales ex-Autos & Gas: 0.0% vs. +0.3% prior

Control Group Sales: -0.1% vs. +0.4% prior

“The consumer isn’t collapsing, but spending is clearly normalizing after a period of outsized resilience.”

U.S. Unemployment Rate

The U.S. unemployment rate declined to 4.3% in January, down from 4.4% in December and slightly better than expectations, signaling continued stability in the labor market despite moderating economic momentum.

Total employment increased by 528,000, while the number of unemployed Americans fell by 141,000 to 7.36 million. Labor force participation also improved modestly to 62.5%, reflecting steady worker re-entry. Encouragingly, the broader U-6 unemployment rate – which captures underemployment – dropped to 8.0% from 8.4%, pointing to improving labor utilization beneath the surface.

Economists expect the following this week:

Unemployment Rate: 4.3% vs. 4.4% prior

Labor Force Participation: 62.5% vs. 62.4% prior

U-6 Unemployment Rate: 8.0% vs. 8.4% prior

“The labor market continues to cool gradually without showing signs of significant deterioration.”

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

This content is sponsored by NEOS Investments. The creator is compensated by NEOS to discuss NEOS ETFs. This content is for informational purposes only, and is not personalized investment, tax, or legal advice, and does not constitute an offer to buy or sell any security. Investing involves risk, including possible loss of principal. Before investing, carefully review the NEOS ETFs prospectus at neosfunds.com.

Grit is a publisher of financial information, not an investment advisor. Grit does not provide personalized or individualized investment advice or information that is tailored to the needs of any particular recipient. Grit does not guarantee the accuracy or completeness of the information provided in this page. All statements and expressions herein are the sole opinion of the author or paid advertiser.

Cover Image Source: James Martin | CNET

THE INFORMATION CONTAINED ON THIS WEBSITE IS NOT AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE, AND DOES NOT PURPORT TO BE AND DOES NOT EXPRESS ANY OPINION AS TO THE PRICE AT WHICH THE SECURITIES OF ANY COMPANY MAY TRADE AT ANY TIME. THE INFORMATION AND OPINIONS PROVIDED HEREIN SHOULD NOT BE TAKEN AS SPECIFIC ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. INVESTORS SHOULD MAKE THEIR OWN INVESTIGATION AND DECISIONS REGARDING THE PROSPECTS OF ANY COMPANY DISCUSSED HEREIN BASED ON SUCH INVESTORS’ OWN REVIEW OF PUBLICLY AVAILABLE INFORMATION AND SHOULD NOT RELY ON THE INFORMATION CONTAINED HEREIN. INVESTORS SHOULD OBTAIN INDIVIDUAL INVESTMENT ADVICE BASED ON THEIR OWN CIRCUMSTANCES BEFORE MAKING AN INVESTMENT DECISION

No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned.

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Any projections, market outlooks or estimates herein are forward looking statements and are inherently unreliable. They are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities discussed herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and Grit undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional material.

Grit does not accept any liability whatsoever for any direct or consequential loss, however arising, directly or indirectly, from any use of the information contained herein.

By using the Site or any related social media account, you are indicating your consent and agreement to this disclaimer and our terms of use. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Please read: Terms of Use, Privacy Policy, Disclosure Policy and Disclaimer Policy

If you have any questions please contact us at [email protected]