- GRIT

- Posts

- 👉 Earnings Reports Return Amid War Issues

Together with Equable Shares

Welcome to your new week.

During crazy times like these, it’s best to stay well-informed. If you want full access to our Week in Review editions, monthly livestreams , portfolio access, monthly stock deep dives, and more — consider upgrading your subscription.

Let’s dive right in.

Equity Investing Doesn’t Have to Be All-or-Nothing

Equable Shares and their Hedged Equity ETF (HEDG) is an actively managed strategy designed to seek long-term capital appreciation while incorporating an options-based hedge to help mitigate downside risk.

In a market environment where volatility can test even disciplined investors, HEDG is designed to offer:

Exposure to large-cap U.S. equities

A structured options overlay

A strategy built around risk management

Built-in downside protection

For investors looking to balance growth potential with a more measured risk profile, HEDG seeks to provide an alternative approach to traditional equity investing.

Explore the strategy at equableshares.com/fund/HEDG.

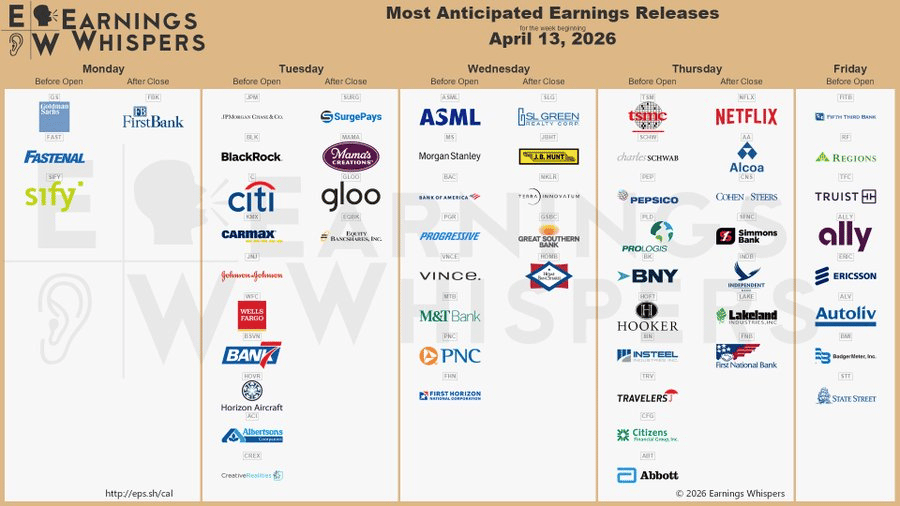

Key Earnings Announcements:

ASML, BlackRock, Goldman Sachs, Netflix, PepsiCo and TSMC highlight this week.

Monday (4/13): Goldman Sachs, Fastenal

Tuesday (4/14): BlackRock, Citi, Johnson & Johnson, Wells Fargo, Bank of New York Mellon

Wednesday (4/15): ASML, Morgan Stanley, Bank of America, Progressive, PNC

Thursday (4/16): TSMC, Netflix, Pepsico, Prologis, Travelers, Abbott

Friday (4/17): Regions Financial, Ally Financial, State Street, Ericsson

What We’re Watching:

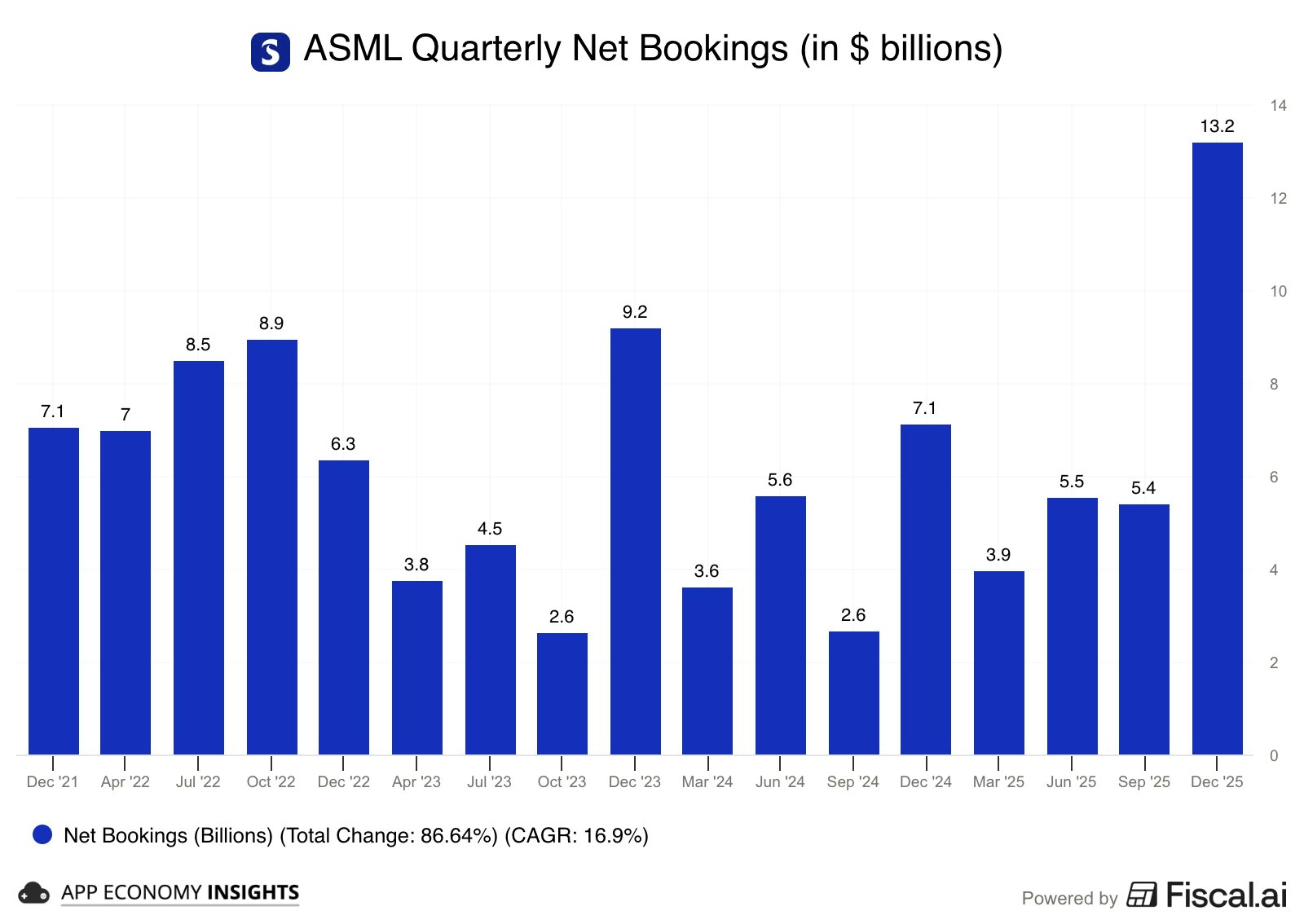

ASML (ASML)

ASML (+38.1% YTD) reports Q1 earnings this week, with investors focused on whether demand for advanced lithography systems — particularly tied to AI and leading-edge chip production — can offset ongoing weakness in parts of the broader semiconductor cycle.

ASML remains a critical supplier to the global chip industry, with its EUV (extreme ultraviolet) machines enabling the most advanced semiconductors used in AI, data centers, and high-performance computing. While AI-driven demand has been a major tailwind, the company has also faced cyclical softness in memory and legacy chips, creating a more uneven demand environment.

Last quarter, ASML delivered solid results with a strong order backlog and continued strength in advanced logic demand, though management flagged variability in the timing of customer orders and installations.

Heading into this release, I’ll be watching for order intake trends, EUV system demand, and commentary on 2026 semiconductor spending, particularly from major customers like TSMC, Samsung, and Intel. Updates on China exposure and export restrictions will also be closely monitored given ongoing geopolitical pressures.

“AI is the key driver behind the current semiconductor upcycle, and it is driving demand across the entire value chain.”

ASML (ASML) Stock Performance, 5-Year Chart, Seeking Alpha

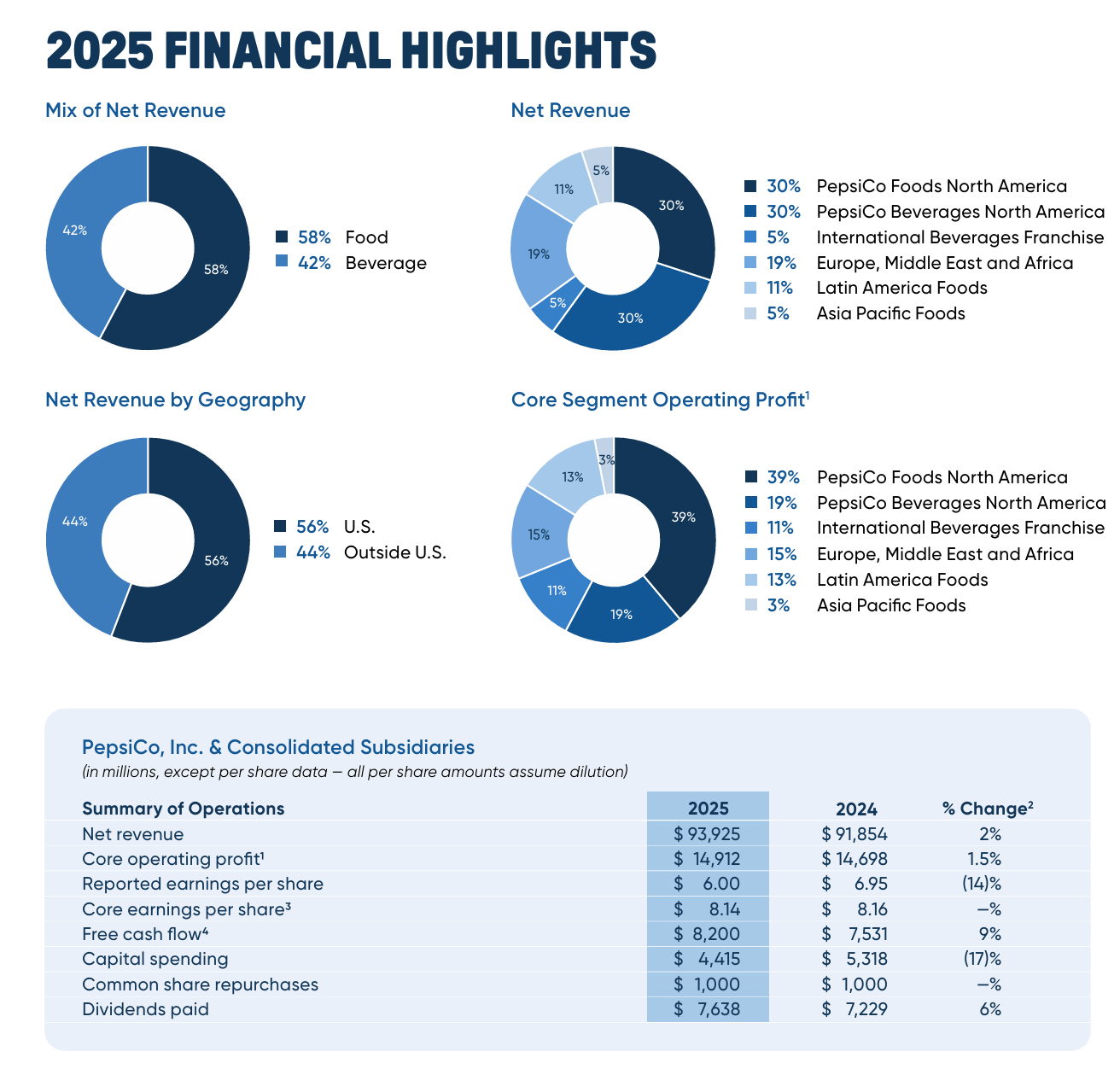

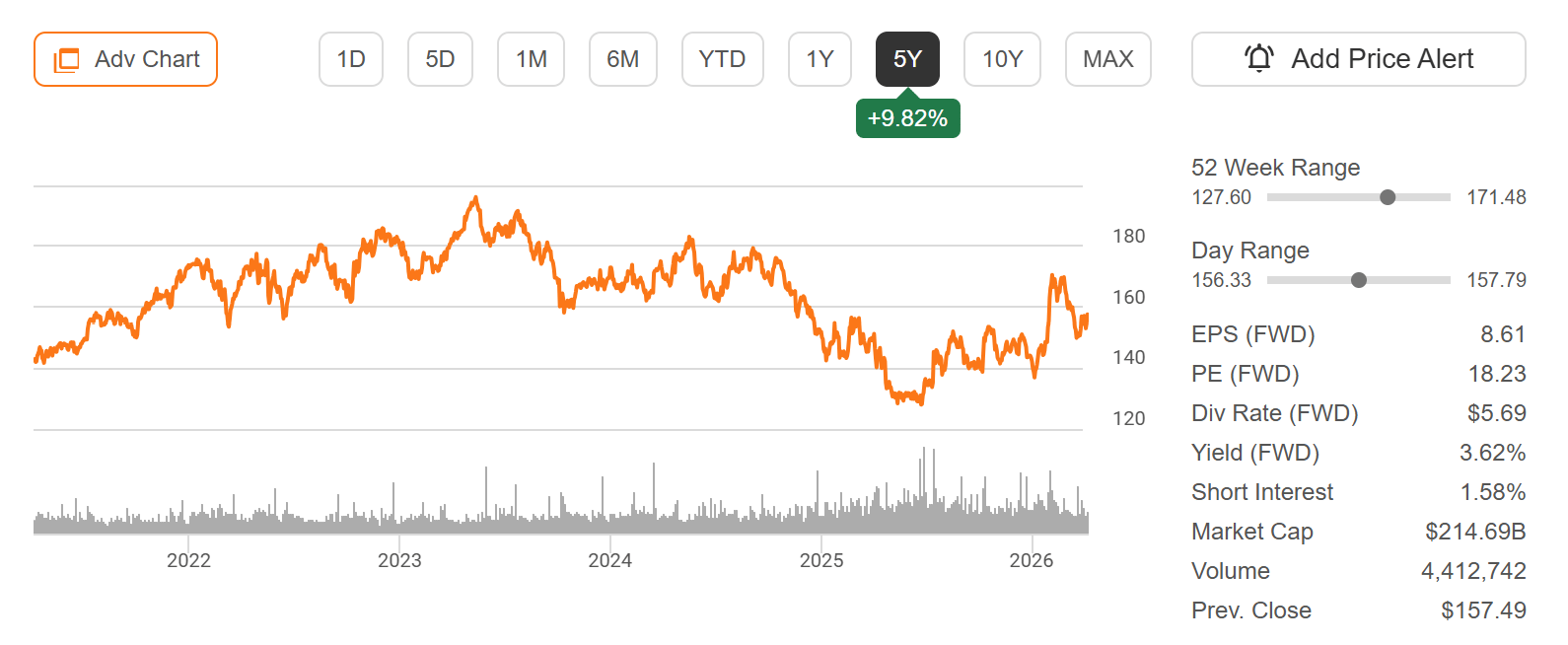

Pepsico (PEP)

Source: Pepsi Investor Relations

PepsiCo (+9.4% YTD) reports Q1 earnings this week, with investors focused on whether the company can sustain its pricing power and volume trends as consumers grow more price-sensitive.

PepsiCo has been a standout within consumer staples, leveraging strong brand equity, international growth, and disciplined pricing to drive steady top-line expansion. However, after multiple quarters of price-led growth, the market is increasingly watching for signs of volume pressure, particularly in North America as consumers trade down or shift spending.

Last quarter, PepsiCo delivered solid results with continued strength in its snacks business (Frito-Lay) and resilient international demand, though management flagged a more cautious consumer backdrop and moderating growth expectations heading into 2026.

Heading into this print, I’ll be watching for commentary on volume vs. pricing mix, margin trends amid input cost volatility, and demand elasticity across key categories like beverages and snacks. Updates on international performance and emerging markets will also be key as PepsiCo looks to offset slower domestic growth.

“Our business remains resilient, supported by the strength of our brands and the continued adaptability of our portfolio.”

Pepsico (PEP) Stock Performance, 5-Year Chart, Seeking Alpha

Investor Events / Global Affairs:

Space symposium highlights growing defense & commercial space opportunity, and the U.S. maritime blockade on Iran signals further escalation.

Space Symposium Highlights Growing Defense & Commercial Space Opportunity

Source: Space Symposium

The annual Space Symposium kicks off this week, bringing together leaders from government, defense, commercial space, and research organizations to discuss the next phase of space exploration and security.

Major defense contractors including Northrop Grumman and Lockheed Martin are set to participate, with markets watching closely for updates on space-based defense systems, satellite infrastructure, and long-term government contract pipelines.

This year’s conference carries added importance following momentum from the Artemis program and expectations for increased global defense spending, particularly as space becomes a more critical domain for national security and technological competition.

For investors, the event serves as a key checkpoint on how governments and private companies are positioning for the next wave of space investment, with implications across aerospace, defense budgets, and emerging commercial space opportunities.

“They can look for rover displays, moon rovers. They can look for, they will see lunar landers. They will see AI technology and capabilities.”

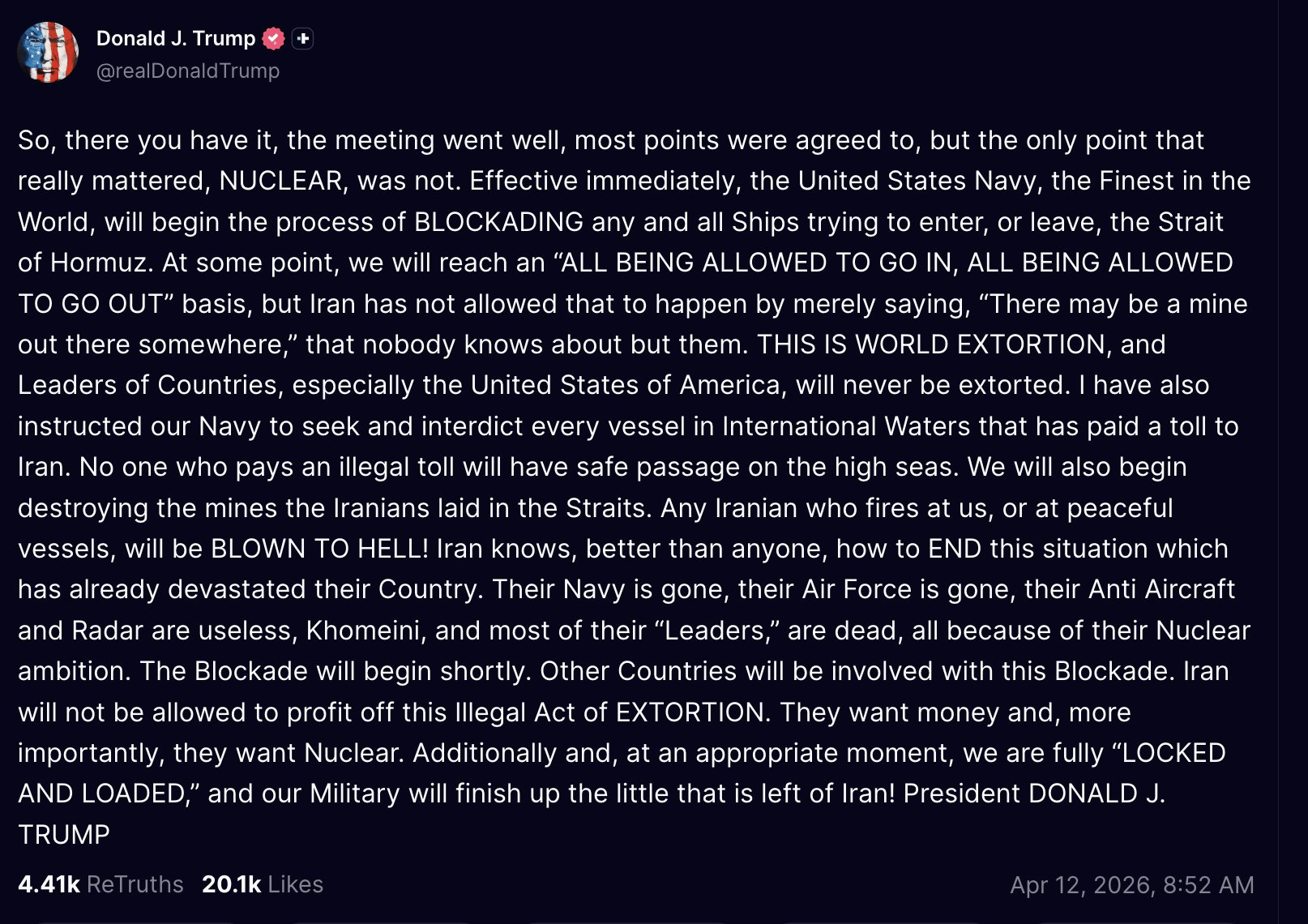

U.S. Maritime Blockade on Iran Signals Further Escalation

Source: Truth Social

The United States Central Command announced it will begin enforcing a maritime blockade on Iranian ports starting April 13, following a directive from Donald Trump, marking a significant escalation in the ongoing conflict.

The blockade will apply to all vessels traveling to or from Iranian ports, including along the Arabian Gulf and Gulf of Oman, while U.S. officials emphasized that freedom of navigation through the Strait of Hormuz will remain open for ships not tied to Iran. Additional guidance is expected to be issued to commercial operators as enforcement begins.

For markets, the move introduces a new layer of risk to global shipping flows and energy supply chains. While the Strait itself remains open, restricting access to Iranian ports could still tighten regional oil exports, disrupt trade routes, and increase insurance and transportation costs across global shipping networks.

Investors will be watching closely for how Iran responds, whether enforcement leads to broader naval tensions, and how quickly these developments feed into oil prices, inflation expectations, and overall risk sentiment.

“The restrictions imposed by criminal America on maritime navigation and transit in international waters are illegal and constitute an example of piracy.”

Major Economic Events:

Fed speak, empire state manufacturing, and PPI highlight this week.

Source: Yahoo Finance

Monday (4/13): Existing home sales, Fed Gov. Stephen Miran speaks

Tuesday (4/14): Core PPI, Fed Gov. Michael Barr speaks, NFIB optimism index, PPI

Wednesday (4/15): Empire State manufacturing survey, Fed Beige Book, Fed Gov. Michael Barr speaks, Homebuilder confidence, Import price index

Thursday (4/16): Capacity utilization, Fed Gov. Stephen Miran speaks, Industrial production, Initial jobless claims, New York Fed President John Williams speaks, Philly Fed manufacturing survey

Friday (4/17): Fed Gov. Christopher Waller speaks, Richmond Fed President Tom Barkin speaks, San Francisco Fed President Mary Daly speaks

What We’re Watching:

Empire State Manufacturing Survey

The NY Empire State Manufacturing Index fell sharply to -0.2 in March, down from 7.1 in February and well below expectations of 3.2, signaling a stall in regional manufacturing activity.

Beneath the headline, the data painted a mixed picture. New orders continued to grow modestly, but shipments declined, pointing to softer near-term output. At the same time, unfilled orders increased and delivery times lengthened, suggesting ongoing supply chain frictions.

On the labor front, conditions remained stable, with modest gains in employment and hours worked, while inventories held relatively steady. Encouragingly, input price pressures eased notably, though they remain elevated, while selling prices were largely unchanged.

Looking ahead, firms maintained a relatively optimistic outlook, with future expectations still positive and capital spending plans improving, indicating confidence in longer-term demand despite near-term volatility.

Economists expect the following this week:

Empire State Index: -0.2 vs. 7.1 prior

New Orders: 6.4 vs. 5.8 prior

Shipments: -6.9 vs. -1.0 prior

“Manufacturing activity held steady in New York State in March. Delivery times lengthened and supply availability worsened slightly. Firms remained optimistic about the outlook.”

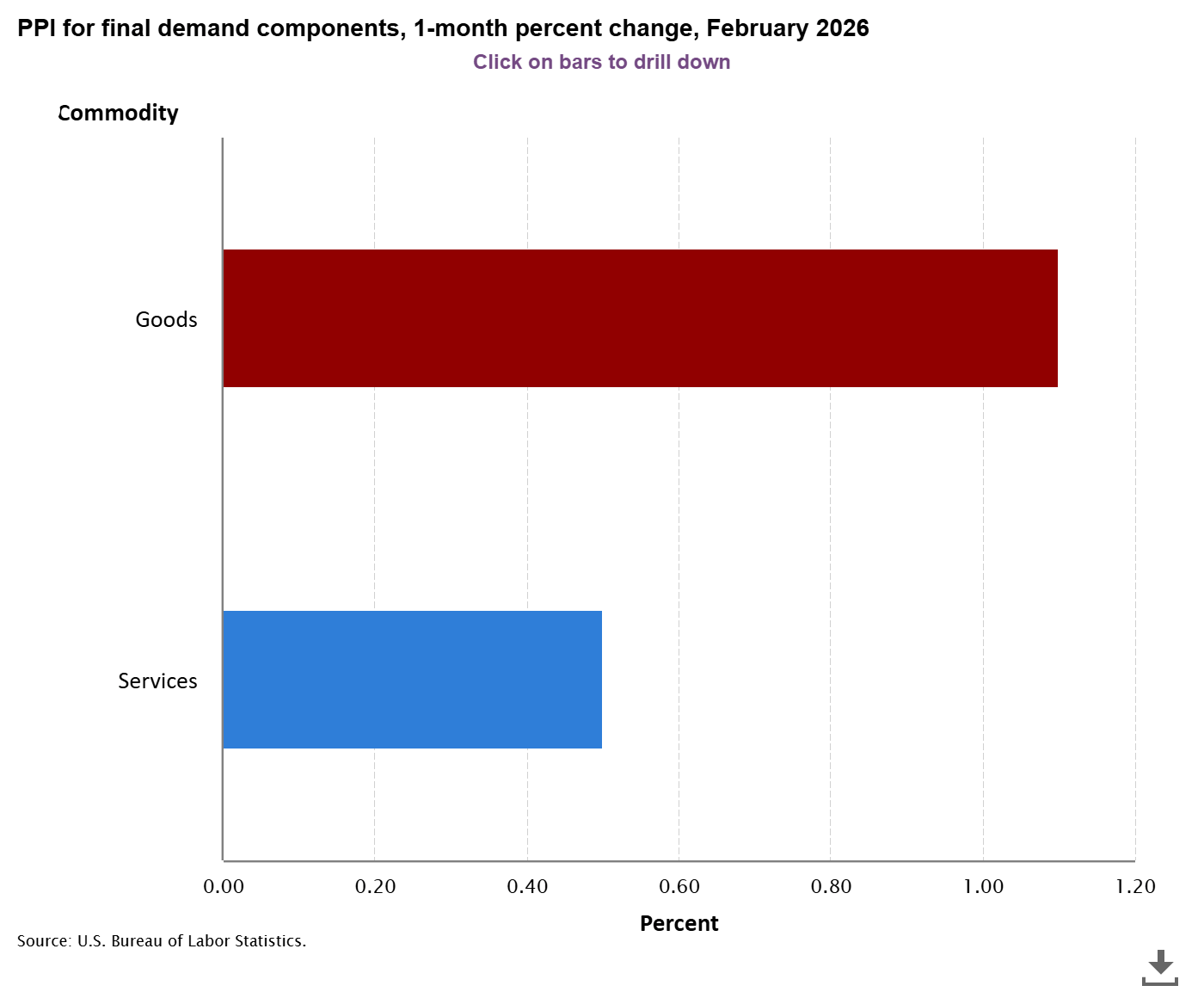

Producer Price Index

U.S. producer prices rose 0.7% MoM in February, accelerating from 0.5% in January and well above expectations of 0.3%, marking the largest monthly increase in seven months. The upside surprise was driven primarily by goods inflation, which surged 1.1%, the strongest gain since August 2023.

Food and energy components led the move higher, including a sharp spike in vegetable prices (+48.9%), alongside increases in diesel, gasoline, jet fuel, and tobacco. While some categories like jewelry and home heating oil declined, the broader trend points to renewed cost pressures at the producer level.

Services inflation was more moderate, rising 0.5%, with strength in travel-related categories such as accommodation. Meanwhile, core PPI increased 0.5%, above expectations, following a strong 0.8% gain in January.

On an annual basis, headline PPI accelerated to 3.4%, the highest in a year, while core PPI rose to 3.9%, reinforcing concerns that underlying inflation remains sticky.

Economists expect the following this week:

Headline PPI (MoM): +0.7% vs. +0.5% prior

Core PPI (MoM): +0.5% vs. +0.3% expected

Headline PPI (YoY): 3.4% vs. 2.9% prior

“The global rise in commodity and energy prices triggered by the war in the Middle East has pushed up producer prices in China through imported inflation.”

Important Disclosures: Investors should carefully consider the investment objectives, risks, charges and expenses of the Fund before investing. The prospectus contains this and other important information and can be obtained at equableshares.com. Please read it carefully before investing. Investing involves risk, including possible loss of principal. Distributed by Quasar Distributors, LLC.

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Grit is a publisher of financial information, not an investment advisor. Grit does not provide personalized or individualized investment advice or information that is tailored to the needs of any particular recipient. Grit does not guarantee the accuracy or completeness of the information provided in this page. All statements and expressions herein are the sole opinion of the author or paid advertiser.

Cover Image Source: Reuters

THE INFORMATION CONTAINED ON THIS WEBSITE IS NOT AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE, AND DOES NOT PURPORT TO BE AND DOES NOT EXPRESS ANY OPINION AS TO THE PRICE AT WHICH THE SECURITIES OF ANY COMPANY MAY TRADE AT ANY TIME. THE INFORMATION AND OPINIONS PROVIDED HEREIN SHOULD NOT BE TAKEN AS SPECIFIC ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. INVESTORS SHOULD MAKE THEIR OWN INVESTIGATION AND DECISIONS REGARDING THE PROSPECTS OF ANY COMPANY DISCUSSED HEREIN BASED ON SUCH INVESTORS’ OWN REVIEW OF PUBLICLY AVAILABLE INFORMATION AND SHOULD NOT RELY ON THE INFORMATION CONTAINED HEREIN. INVESTORS SHOULD OBTAIN INDIVIDUAL INVESTMENT ADVICE BASED ON THEIR OWN CIRCUMSTANCES BEFORE MAKING AN INVESTMENT DECISION

No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned.

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Any projections, market outlooks or estimates herein are forward looking statements and are inherently unreliable. They are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities discussed herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and Grit undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional material.

Grit does not accept any liability whatsoever for any direct or consequential loss, however arising, directly or indirectly, from any use of the information contained herein.

By using the Site or any related social media account, you are indicating your consent and agreement to this disclaimer and our terms of use. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Please read: Terms of Use, Privacy Policy, Disclosure Policy and Disclaimer Policy

If you have any questions please contact us at [email protected]