- GRIT

- Posts

- 👉 Everything Rides on Nvidia

In partnership with

Welcome to your new week.

Positive and negative AI news is constant, Trump’s tariffs are back at the forefront, and the entire market is anxiously awaiting Nvidia’s earnings.

Read on for a quick preview of everything you should know this week.

Key Earnings Announcements:

Plain and simple — all eyes are on Nvidia.

Monday (2/23): BWX Technologies, Diamondback Energy, Dominion Energy, Freshpet, Hims & Hers, Keysight Technologies, Kratos Defense, ONEOK

Tuesday (2/24): AMC Entertainment, Axon Enterprise, Cava Group, DigitalOcean, FIS, MercadoLibre, Navitas Semiconductor, Workday

Wednesday (2/25): BMO, Hut 8, IONQ, Ionis Pharmaceuticals, NVIDIA, Salesforce, Snowflake, Synopsys, TJX Companies, VICI Properties

Thursday (2/26): ACM Research, Baidu, CoreWeave, Dell Technologies, Duolingo, Marathon Digital, Pure Storage, Warner Bros. Discovery, Zscaler

Friday (2/27): Amneal Pharmaceuticals, Arbor Realty Trust, Endeavour Silver, NW Natural, Sunstone Hotel Investors, V2X

What We’re Watching:

Nvidia (NVDA)

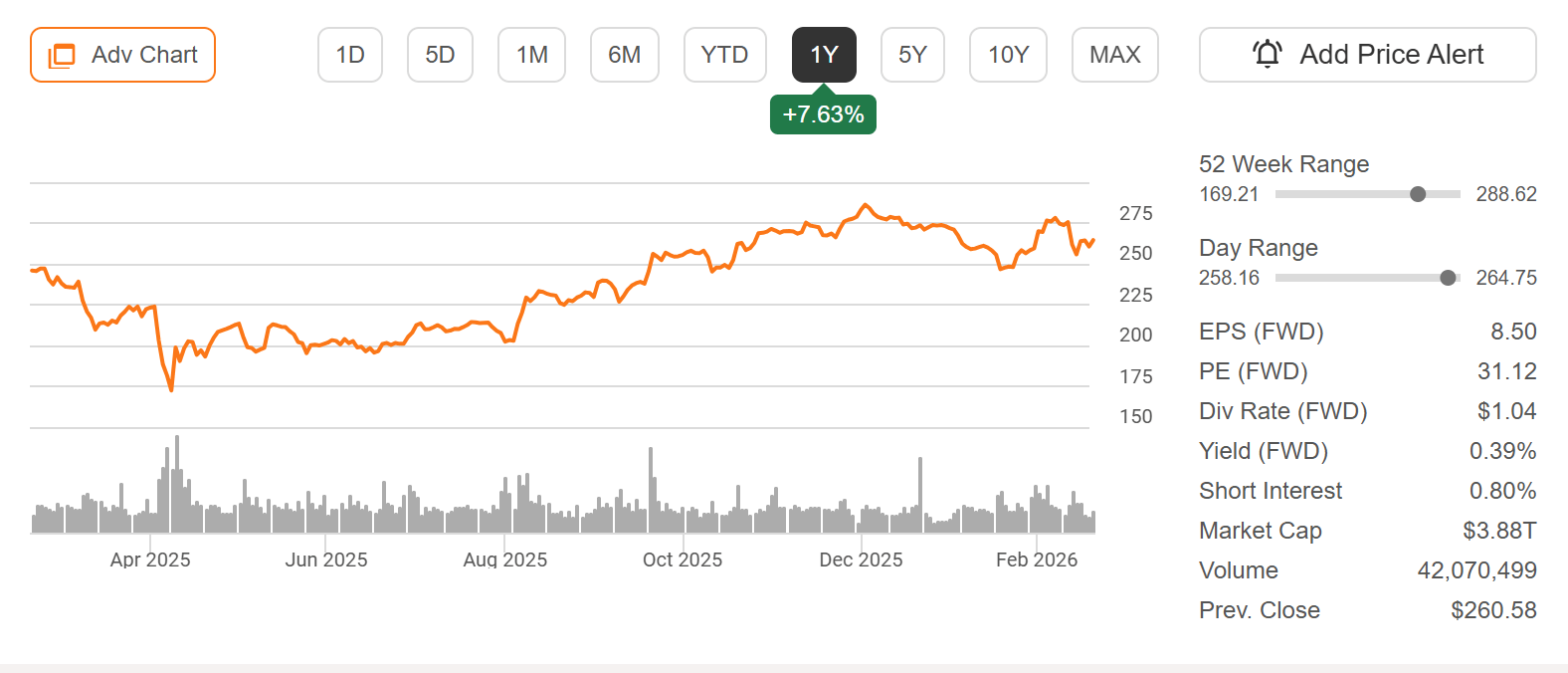

Nvidia (+1.8% YTD) reports Q4 FY2025 earnings this week, one of the most consequential tech prints of the quarter as markets weigh AI demand, margin sustainability, and capital-spending cadence across data centers and enterprise technology.

Nvidia has been the poster child of the AI bull market, powering generative AI deployments with its GPU and accelerator portfolio.

Last quarter, the company reported revenue well above expectations with premium data-center growth, strong OEM engagement, and solid graphics performance underpinning results. But sentiment has cooled from the frothy highs of 2023–24, and investors are now asking whether demand remains durable amid rising competition, inventory normalization, and broader tech selloffs.

Heading into this print, I’ll be watching several critical themes:

Data-center revenue trajectory — especially AI-GPU sales and cloud partner demand

Gross margin sustainability as ASPs cycle and mix shifts toward next-gen products

Guidance for 2026 capex and AI infrastructure spending — signaling whether customers are stepping up or pausing

Inventory and channel checks — particularly around hyperscaler ordering patterns

“The AI transition represents a once-in-a-generation replatforming of computing – and Nvidia’s ecosystem remains central to that transformation.”

Nvidia Corporation (NVDA) Stock Performance, 5-Year Chart, Seeking Alpha

The Architecture Behind AI-Native Revenue Automation

Most “AI finance” tools guess. Finance can’t. This white paper explains how AI-native revenue automation combines reasoning, deterministic math, and commercial context to automate billing, cash, and close—without sacrificing accuracy. Read the architecture behind AI-native revenue automation.

Salesforce (CRM)

Salesforce reports Q4 FY2025 earnings this week amid a challenging backdrop for software stocks, with concern over AI disruption contributing to a roughly -30% YTD decline in its share price. Investors will be watching whether the CRM leader can demonstrate durable demand and monetization as AI hype, sentiment swings, and competitive disruption pressure valuations across the tech sector.

Last quarter, Salesforce delivered $9.8 billion in revenue (+14% YoY) and $1.50 in adjusted EPS (+18% YoY), beating expectations as strength in Sales Cloud, Service Cloud, and AI-driven automation lifted recurring revenue. Management also highlighted continued momentum in digital transformation initiatives and expanding AI usage across its platform.

Heading into this print, I’ll be focused on whether subscription revenue trends hold up in the face of industry-wide software multiple compression, if AI-related product adoption — such as Einstein and Slack integrations — is translating into meaningful ARR acceleration, and how forward guidance reflects customers’ willingness to invest in enterprise tech and AI amid macro uncertainties.

“Our customers are accelerating their digital transformations with AI at the center – and we’re seeing that reflected in both pipeline and retention.”

Salesforce, Inc. (CRM) Stock Performance, 5-Year Chart, Seeking Alpha

Investor Events / Global Affairs:

Apple annual meeting puts China exposure in focus, JPMorgan to host investor update in NYC, and Supreme Court tariff ruling creates fresh business uncertainty.

Apple Annual Meeting Puts China Exposure in Focus

Apple (APPL) Stock Performance, 1-Year Chart, Seeking Alpha

Apple will hold its annual shareholder meeting this week, with attention centered on a proposal requesting a board-level report on the risks and costs tied to the company’s operations in China. The measure — submitted by the National Center for Public Policy Research — calls for greater transparency around supply-chain concentration, tariff exposure, access to rare earth materials, and broader security considerations.

Shareholders will also vote on director re-elections, including board chair Art Levinson and director Ron Sugar, for whom the board has waived its customary age-75 retirement guideline.

While the proposals are unlikely to materially alter near-term operations, the discussion underscores ongoing geopolitical scrutiny around China exposure – a factor that remains central to Apple’s manufacturing footprint and long-term risk profile.

“As part of Apple's meeting on February 24, participants will vote on the election of its Board of Directors and will ratify the appointment of Apple's independent registered public accounting firm for 2026. Participants will also vote on Apple's Non-Employee Director Stock Plan, executive compensation, and a shareholder proposal related to Apple's manufacturing efforts in China.”

JPMorgan to Host Investor Update in NYC

JPMorgan Chase (JPM) Stock Performance, 1-Year Chart, Seeking Alpha

JPMorgan Chase will host a company update in New York City this week, with investors focused on a more detailed firm-wide review than in recent years. CFO Jeremy Barnum is expected to provide a deeper breakdown across major business lines – including consumer banking, investment banking, markets, and asset & wealth management.

The event will conclude with prepared remarks and Q&A from CEO Jamie Dimon, whose commentary on credit trends, capital allocation, regulatory outlook, and macro conditions will be closely watched.

With bank stocks sensitive to rate expectations and credit quality, any updates on loan growth, net interest income guidance, or capital return plans could move the group.

“JPMorgan Chase acknowledged for the first time that it closed the bank accounts of President Donald Trump and several of his businesses in the political and legal aftermath of the Jan. 6, 2021, attacks on the U.S. Capitol, the latest development in a legal saga between the president and the nation’s biggest bank over the issue known as “debanking.”

The acknowledgment came in a court filing submitted this week in Trump’s lawsuit against the bank and its leader, Jamie Dimon. The president sued for $5 billion, alleging that his accounts were closed for political reasons, disrupting his business operations.”

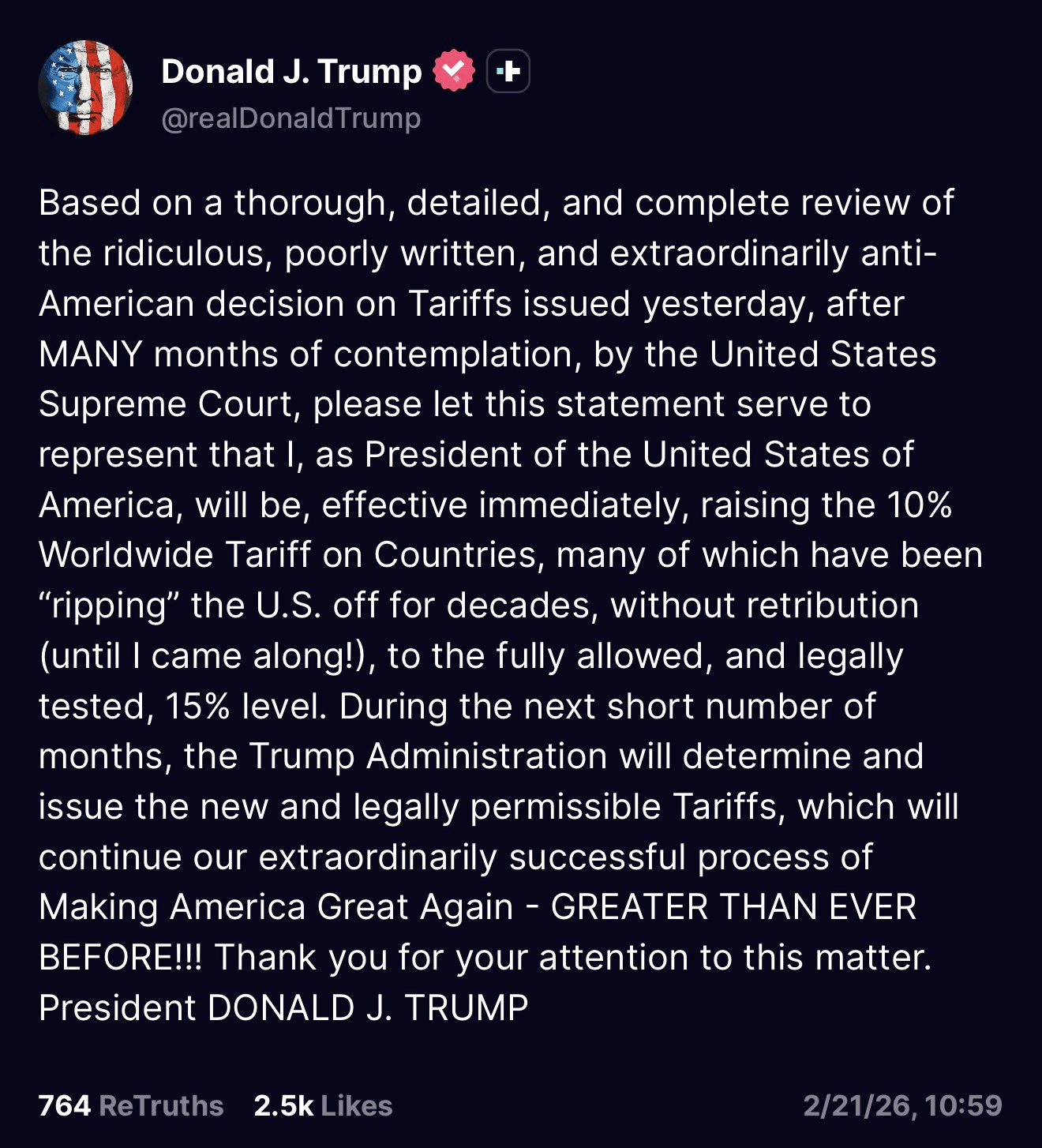

Supreme Court Tariff Ruling Creates Fresh Business Uncertainty

The Supreme Court struck down key elements of President Trump’s signature tariffs, but the decision has left corporate America with more questions than clarity. While companies welcomed the ruling, uncertainty remains around whether previously paid tariffs will be refunded – and how quickly.

Business leaders are now evaluating potential refund litigation, pricing adjustments, and the impact of President Trump’s announcement of a new 15% global tariff under separate legal authority. Trade groups are pushing for streamlined refunds, but Treasury officials have suggested any recovery process could take months or longer.

Executives across retail, manufacturing, and consumer goods are weighing whether to alter supply chains, adjust pricing, or hold steady amid continued policy volatility. Many larger multinationals have already built modeling teams and “war rooms” to simulate tariff outcomes, while smaller businesses face more immediate cash-flow pressure.

For markets, the key issues this week are:

Whether refund mechanisms become clearer

The scope and timing of newly announced tariffs

How companies adjust guidance amid policy shifts

“Fiscal conditions already point to a sizable positive impulse in 2026, driven by the One Big Beautiful Bill Act and an easing monetary policy backdrop. The tariff ruling may incrementally enhance this stimulus, reinforcing expectations for above-trend economic growth.”

Major Economic Events:

Factory orders, initial jobless claims, and producer price index highlight this week.

Monday (2/23): Factory orders, Fed Governor Christopher Waller speaks

Tuesday (2/24): Atlanta Fed President Raphael Bostic speaks, Chicago Fed President Austan Goolsbee speaks, Consumer confidence, Fed Governor Christopher Waller speaks, Fed Governor Lisa Cook speaks, S&P Case-Shiller Home Price Index (20 cities), Wholesale inventories

Wednesday (2/25): Kansas City Fed President Jeffrey Schmid speaks, Richmond Fed President Tom Barkin speaks

Thursday (2/26): Initial jobless claims

Friday (2/27): Chicago Business Barometer (PMI), Construction spending (Dec), Construction spending (Nov delayed), Core PPI, Core PPI year over year, PPI year over year, Producer Price Index (delayed report)

What We’re Watching:

Initial Jobless Claims

Initial jobless claims fell by 23,000 to 206,000 in the second week of February, well below expectations of 225,000 and returning to levels comfortably below early-2025 averages. The drop reinforces the view that layoffs remain contained despite softer hiring momentum across several sectors.

Continuing claims – a measure of ongoing unemployment – edged up modestly by 17,000 to 1.87 million, suggesting that while job losses remain limited, reemployment may be taking slightly longer. Overall, the data points to a labor market that is cooling gradually but not deteriorating – consistent with the Federal Reserve’s characterization of a “balanced” employment backdrop.

Economists expect the following this week:

Initial Jobless Claims: 206K vs. 229K prior

Continuing Claims: 1.87M vs. 1.85M prior

“I think you can say that the labor market has continued to cool gradually, maybe just a touch more gradually than we thought.”

Producer Price Index

U.S. producer prices rose +0.5% MoM in December, the largest monthly increase in three months and well above expectations for +0.2%. The upside surprise was driven primarily by services, which rebounded +0.5% after being flat in November, led by a sharp increase in machinery and equipment wholesaling margins.

Goods prices were flat overall, though there were notable swings beneath the surface. Nonferrous metals surged +4.5%, and prices rose for natural gas, motor vehicles, soft drinks, and aircraft equipment. Offsetting those gains, diesel fuel plunged 14.6%, with declines also seen in gasoline, jet fuel, beef, and scrap metals.

Core PPI – excluding food and energy –jumped +0.7% MoM, the strongest gain since July and well above forecasts. On a yearly basis, headline PPI held at +3.0%, while core producer inflation accelerated to +3.3%, exceeding expectations.

Economists expect the following this week:

Headline PPI (MoM): +0.5% vs. +0.2% prior

Core PPI (MoM): +0.7% vs. 0.0% prior

Core PPI (YoY): 3.3% vs. 3.0% prior

“The larger-than-expected rise in the Producer Price Index last month reported by the Labor Department on Friday was driven by a surge in services, mostly trade services, which measure changes in margins received by wholesalers and retailers. There were also strong increases in the prices of hotel and motel rooms as well as airline fares. But goods prices were unchanged.”

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

This content is sponsored by NEOS Investments. The creator is compensated by NEOS to discuss NEOS ETFs. This content is for informational purposes only, and is not personalized investment, tax, or legal advice, and does not constitute an offer to buy or sell any security. Investing involves risk, including possible loss of principal. Before investing, carefully review the NEOS ETFs prospectus at neosfunds.com.

Grit is a publisher of financial information, not an investment advisor. Grit does not provide personalized or individualized investment advice or information that is tailored to the needs of any particular recipient. Grit does not guarantee the accuracy or completeness of the information provided in this page. All statements and expressions herein are the sole opinion of the author or paid advertiser.

Cover Image Source: World Finance

THE INFORMATION CONTAINED ON THIS WEBSITE IS NOT AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE, AND DOES NOT PURPORT TO BE AND DOES NOT EXPRESS ANY OPINION AS TO THE PRICE AT WHICH THE SECURITIES OF ANY COMPANY MAY TRADE AT ANY TIME. THE INFORMATION AND OPINIONS PROVIDED HEREIN SHOULD NOT BE TAKEN AS SPECIFIC ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. INVESTORS SHOULD MAKE THEIR OWN INVESTIGATION AND DECISIONS REGARDING THE PROSPECTS OF ANY COMPANY DISCUSSED HEREIN BASED ON SUCH INVESTORS’ OWN REVIEW OF PUBLICLY AVAILABLE INFORMATION AND SHOULD NOT RELY ON THE INFORMATION CONTAINED HEREIN. INVESTORS SHOULD OBTAIN INDIVIDUAL INVESTMENT ADVICE BASED ON THEIR OWN CIRCUMSTANCES BEFORE MAKING AN INVESTMENT DECISION

No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned.

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Any projections, market outlooks or estimates herein are forward looking statements and are inherently unreliable. They are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities discussed herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and Grit undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional material.

Grit does not accept any liability whatsoever for any direct or consequential loss, however arising, directly or indirectly, from any use of the information contained herein.

By using the Site or any related social media account, you are indicating your consent and agreement to this disclaimer and our terms of use. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Please read: Terms of Use, Privacy Policy, Disclosure Policy and Disclaimer Policy

If you have any questions please contact us at [email protected]