- GRIT

- Posts

- 👉 Largest Monthly Inflation Increase Since 2022?

👉 Largest Monthly Inflation Increase Since 2022?

Delta, Iran War, JPMorgan's $1T Economic Injection

Austin Hankwitz

06 Apr

Together with WisdomTree

Welcome to your new week.

During crazy times like these, it’s best to stay well-informed. If you want full access to our Week in Review editions, monthly livestreams , portfolio access, monthly stock deep dives, and more — consider upgrading your subscription.

Let’s dive right in.

Position Portfolios for Structural Defense Growth

Geopolitical uncertainty is rising and global defense spending is accelerating alongside it. A multi-year modernization cycle is underway, reshaping the investment landscape beyond short-term headlines.

WisdomTree’s Defense Suite of ETFs provides targeted, globally diversified exposure to companies supporting today’s evolving security needs—from advanced technologies to next-generation defense systems.

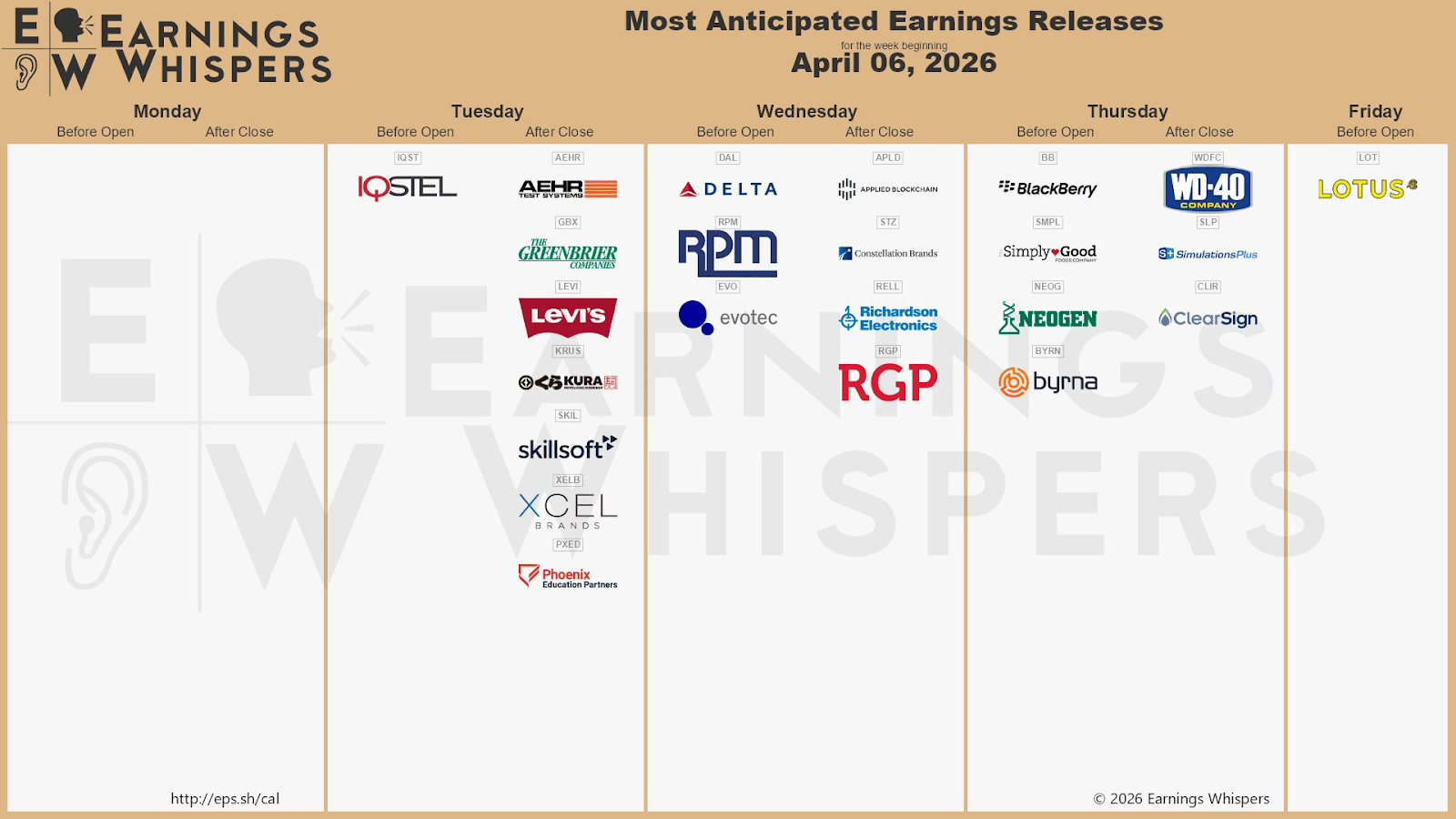

Key Earnings Announcements:

Constellations Brands and Delta highlight this slow week of earnings

Monday (4/6): N/A

Tuesday (4/7): Levi’s

Wednesday (4/8): Constellation Brands, Delta

Thursday (4/9): Blackberry, WD-40

Friday (4/10): N/A

What We’re Watching:

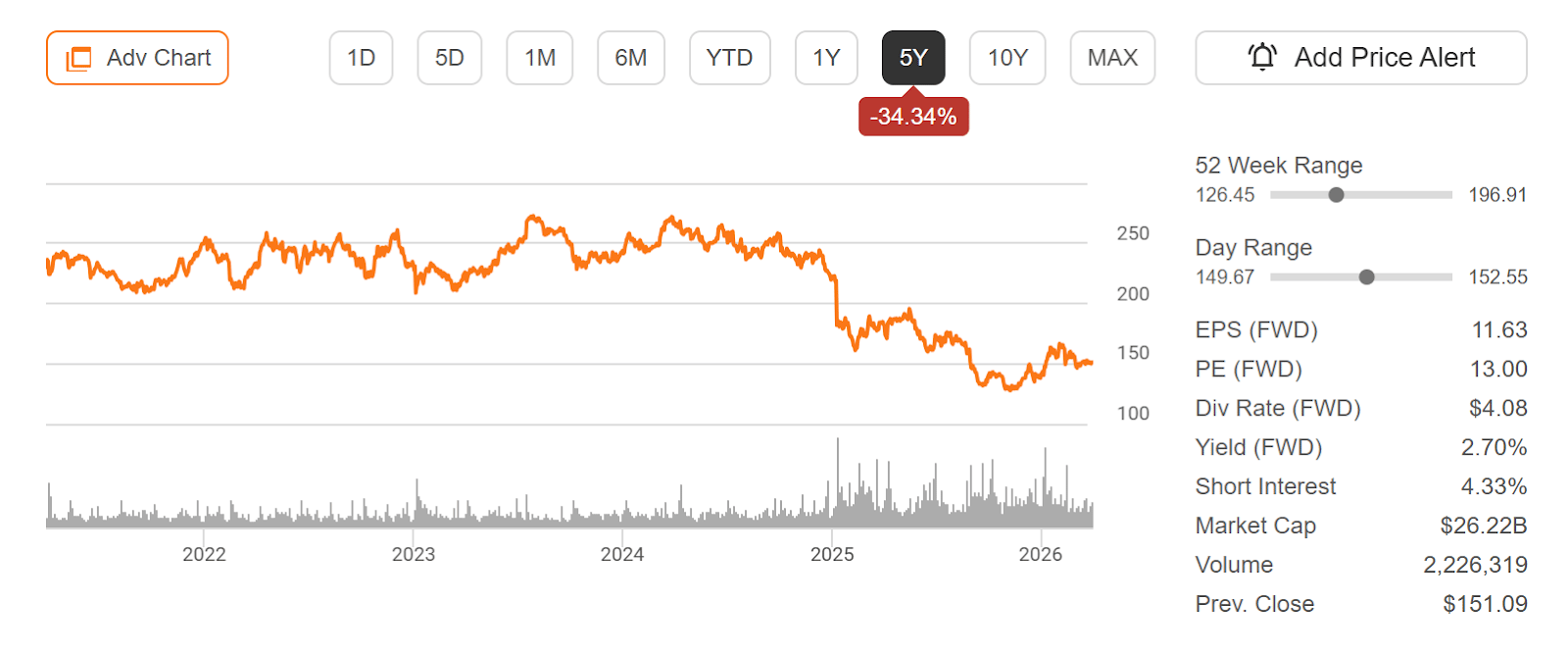

Constellation Brands (STZ)

Constellation Brands (+9.6% YTD) reports earnings this week, with investors focused on demand trends across its beer portfolio and the ongoing reset in its wine and spirits business. The company remains heavily tied to the performance of its Mexican beer brands – Modelo, Corona, and Pacifico – which have been key drivers of growth in recent years.

Recent results have highlighted continued strength in the beer segment, supported by pricing and resilient consumer demand, while the wine and spirits division has faced ongoing pressure from declining volumes and portfolio repositioning. Management has been actively streamlining that business, divesting lower-end brands and shifting focus toward higher-margin offerings.

Key areas of focus this quarter will include beer depletion trends, pricing vs. volume dynamics, and progress within the wine and spirits turnaround. Investors will also be looking for updates on margin trajectory and capital allocation priorities – particularly share buybacks and reinvestment into core brands – as the company works to return to more consistent, profitable growth.

“Our beer business continues to deliver strong, consistent growth, supported by the strength of our core brands and consumer demand.”

Constellation Brands (STZ) Stock Performance, 5-Year Chart, Seeking Alpha

Delta Air Lines (DAL)

Delta Air Lines (+3.8% YTD) reports earnings this week, with investors focused on how rising fuel costs and geopolitical tensions are impacting margins heading into peak travel season. The print comes as oil prices have surged amid the Iran conflict, creating a more challenging cost backdrop for airlines that are highly sensitive to energy prices.

Last quarter, Delta delivered solid results supported by strong premium and international travel demand, with higher-margin segments helping offset cost pressures. The company has continued to emphasize its premium offerings and diversified revenue streams, which have allowed it to outperform many peers despite a more volatile macro environment.

I’ll be watching for commentary on fuel cost pressures, pricing power, and whether premium travel demand remains resilient. Updates to full-year guidance and any signals around capacity or demand trends into the summer travel season will be key as investors assess whether Delta can maintain margins in a higher-cost environment.

“We continue to see resilient demand for premium travel, even as we navigate a more volatile cost environment driven by fuel.”

Delta Air Lines (DAL) Stock Performance, 5-Year Chart, Seeking Alpha

Investor Events / Global Affairs:

Geopolitics remain the primary influence on the market, JPMorgan is injecting $1 trillion into the US economy, and the HumanX AI Conference will take place in San Francisco this week.

Geopolitics in Control of the Market

Today marks Day 37 of the Iran War. U.S. equity futures went lower over the weekend (before rebounding to begin the week) as President Trump escalated rhetoric, declaring Tuesday “Power Plant and Bridge Day” in Iran — signaling potential targeting of critical infrastructure. At the same time, oil markets reacted sharply, with crude surging above $114/barrel as supply concerns intensified following the long weekend.

The backdrop remains highly fragile: shipping disruptions through key energy routes persist, infrastructure risks are rising, and each headline continues to drive outsized moves across commodities, equities, and rates.

Markets are now trading geopolitics first, with energy prices acting as the primary transmission mechanism into inflation expectations and risk sentiment. Any further escalation — or signs of de-escalation — could quickly shift the macro narrative.

“Iran does not hesitate to clearly express what it considers its legitimate demands and doing so should not be interpreted as a sign of compromise, but rather as a reflection of its confidence in defending its positions.”

JPMorgan to Deploy $1 Trillion to Strengthen US Economy

Source: Tom Williams/CQ-Roll Call, Inc/Getty Images

Jamie Dimon warned that the U.S. must “get stronger” economically and militarily to maintain its global leadership, emphasizing that no country is guaranteed long-term success. He highlighted JPMorgan Chase’s plan to deploy over $1 trillion in capital toward strengthening the U.S. economy — targeting areas like infrastructure, supply chains, energy security, and broader economic resilience over the next decade.

This includes initiatives like the American Dream Initiative, focused on expanding economic opportunity, alongside a broader push to support industries critical to national security. Dimon’s message is that large institutions must play an active role in shaping policy and investing in the long-term competitiveness of the country — not just maximizing short-term profits.

He also pointed to rising geopolitical risks, particularly the Iran conflict, as a growing threat to global stability and commodity markets. On the financial side, he flagged potential cracks in private credit and private equity, warning that weaker lending standards and extended holding periods could become problematic in a downturn.

The big takeaway: Dimon is positioning JPMorgan not just as a bank, but as a major capital allocator in the next phase of U.S. economic and geopolitical competition.

“We have a responsibility to help shape the right policies, not just for our company but for the country and the world. Many companies will only thrive if their countries thrive.”

HumanX AI Conference

The HumanX AI Conference kicks off this week in San Francisco, featuring a heavyweight lineup including Amazon, Microsoft, NVIDIA, Google, OpenAI, Anthropic, Databricks, and CoreWeave.

The event comes at a key moment for markets as investors look for confirmation that AI spending, infrastructure demand, and enterprise adoption remain durable into 2026. With many of the companies driving the AI cycle in one place, commentary around capex, monetization, and real-world use cases will be closely watched.

“HumanX is an unmissable, high-impact conference that unites 6,500 leaders, builders, and investors driving real transformation. It’s not just panels and hype; at HumanX, every session, meeting, and moment is designed to help you Learn, Connect, and Go—moving from inspiration to execution in just four days.”

Major Economic Events:

We will learn a lot about inflation this week via the CPI and PCE Price Index.

Monday (4/6): ISM services

Tuesday (4/7): Consumer credit, Durable goods orders, Fed Vice Chair Philip Jefferson speaks

Wednesday (4/8): Fed minutes (FOMC), San Francisco Fed President Mary Daly speaks

Thursday (4/9): Core PCE, GDP (second revision), Initial jobless claims, PCE index, Personal income, Personal spending

Friday (4/10): CPI, Core CPI, Consumer sentiment (prelim), Factory orders

What We’re Watching:

Core PCE Price Index

US Core PCE Index Annual Change, 5-Year Chart, Trading Economics

Core PCE rose 0.4% in January and 3.1% year-over-year, remaining well above the Fed’s 2% target. The monthly reading also ticked higher from December, signaling that underlying inflation pressures are not easing as quickly as hoped. Because core PCE strips out food and energy, it’s viewed as a cleaner measure of persistent inflation — making this stickiness more concerning for policymakers. The takeaway: inflation is still running hot beneath the surface, limiting the Fed’s flexibility to cut rates anytime soon.

Economists expect the following this week:

Core PCE Index: +0.4% vs. +0.4% the month prior

Core PCE (year-over-year): +3.0% vs. +3.1% the month prior

"Gasoline prices in the U.S. are poised to rise to around $3.75 per gallon nationally in the coming weeks, and it could take much of the year to trend back to pre-conflict prices near $3 per gallon. The spike in diesel fuel prices will feed into higher transportation costs and could lift price pressures across the supply chain. Further, the disruption of agricultural fertilizer shipments will place upward pressure on food prices."

Consumer Price Index (CPI)

March CPI is expected to come in hot, with forecasts around +1.0% month-over-month and +3.3% year-over-year, driven largely by a sharp surge in gasoline prices. A roughly 35% jump in gas alone could contribute as much as 0.5%–0.6% to the headline number, creating a meaningful near-term inflation spike. Even core CPI is expected to tick higher, suggesting broader price pressures beyond just energy.

For markets, this report is critical. A hotter-than-expected print could force a repricing of rate expectations and keep the Fed on hold — or even push the conversation back toward hikes. Conversely, a cooler reading would likely spark a short-term risk-on rally, but the underlying inflation trend remains a key concern.

Economists expect the following this week:

CPI (monthly): +1.0% vs +0.3% the month prior

CPI (annual): +3.3% vs. +2.4% the month prior

Core CPI (monthly): +0.3% vs. +0.2% the month prior

Core CPI (annual): +2.7% vs. +2.5% the month prior

“Economists project the US Consumer Price Index will jump +1% in March from February, the largest monthly increase since mid-2022, fueled by a steep rise in gasoline prices. This follows a $1 per gallon climb at the pump amid Middle East tensions disrupting oil shipments. Such a spike would mark a major setback for the disinflation trend that had buoyed markets earlier this year.”

WisdomTree Disclosures: Investors should carefully consider the investment objectives, risks, charges and expenses of the Fund before investing. For a prospectus or, if available, the summary prospectus containing this and other important information about the fund, call 866.909.9473 or visit WisdomTree.com/investments. Read the prospectus or, if available, the summary prospectus carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S.

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

This content is sponsored by NEOS Investments. The creator is compensated by NEOS to discuss NEOS ETFs. This content is for informational purposes only, and is not personalized investment, tax, or legal advice, and does not constitute an offer to buy or sell any security. Investing involves risk, including possible loss of principal. Before investing, carefully review the NEOS ETFs prospectus at neosfunds.com.

Grit is a publisher of financial information, not an investment advisor. Grit does not provide personalized or individualized investment advice or information that is tailored to the needs of any particular recipient. Grit does not guarantee the accuracy or completeness of the information provided in this page. All statements and expressions herein are the sole opinion of the author or paid advertiser.

Cover Image Source: Tom Williams/CQ-Roll Call, Inc/Getty Images

THE INFORMATION CONTAINED ON THIS WEBSITE IS NOT AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE, AND DOES NOT PURPORT TO BE AND DOES NOT EXPRESS ANY OPINION AS TO THE PRICE AT WHICH THE SECURITIES OF ANY COMPANY MAY TRADE AT ANY TIME. THE INFORMATION AND OPINIONS PROVIDED HEREIN SHOULD NOT BE TAKEN AS SPECIFIC ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. INVESTORS SHOULD MAKE THEIR OWN INVESTIGATION AND DECISIONS REGARDING THE PROSPECTS OF ANY COMPANY DISCUSSED HEREIN BASED ON SUCH INVESTORS’ OWN REVIEW OF PUBLICLY AVAILABLE INFORMATION AND SHOULD NOT RELY ON THE INFORMATION CONTAINED HEREIN. INVESTORS SHOULD OBTAIN INDIVIDUAL INVESTMENT ADVICE BASED ON THEIR OWN CIRCUMSTANCES BEFORE MAKING AN INVESTMENT DECISION

No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned.

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Any projections, market outlooks or estimates herein are forward looking statements and are inherently unreliable. They are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities discussed herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and Grit undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional material.

Grit does not accept any liability whatsoever for any direct or consequential loss, however arising, directly or indirectly, from any use of the information contained herein.

By using the Site or any related social media account, you are indicating your consent and agreement to this disclaimer and our terms of use. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Please read: Terms of Use, Privacy Policy, Disclosure Policy and Disclaimer Policy

If you have any questions please contact us at [email protected]