- GRIT

- Posts

- 👉 Major Earnings + Big Events

Together with VantagePoint AI

Welcome to your new week.

During market swings, it’s always best to stay well-informed! If you want full access to our Week in Review editions, monthly livestreams , portfolio access, monthly stock deep dives, and more — consider upgrading your subscription.

Let’s dive right in.

AI Solves This for Traders in 15 Minutes

What if finding your next options trade didn’t require hours of chart analysis, scanning dozens of tickers, or second-guessing every move?

This AI does the heavy lifting for you.

Our artificial intelligence processes millions of data points daily across markets, sectors, and intermarket relationships to surface high-probability options setups before the crowd even knows they exist.

No guesswork. No noise. Because you’re given a clear, data-driven direction telling you exactly where to focus.

In our free live training session, our expert will walk you through exactly how the AI forecast model works, and you’ll learn about the specific stocks and options setting up for major moves right now.

Key Earnings Announcements:

American Express, IBM, Intel, RTX, ServiceNow, and Tesla highlight this week.

Monday (4/20): Alaska Air, Steel Dynamics, Wintrust Financial

Tuesday (4/21): UnitedHealth, RTX, 3M, Capital One, Danaher, DR Horton, Halliburton

Wednesday (4/22): Tesla, IBM, AT&T, Boeing, Texas Instruments, ServiceNow, Lam Research

Thursday (4/23): Intel, American Express, Freeport-McMoRan, Lockheed Martin, Dow, Baker Hughes

Friday (4/24): Procter & Gamble, Schlumberger, HCA Healthcare, Norfolk Southern, American Airlines

What We’re Watching:

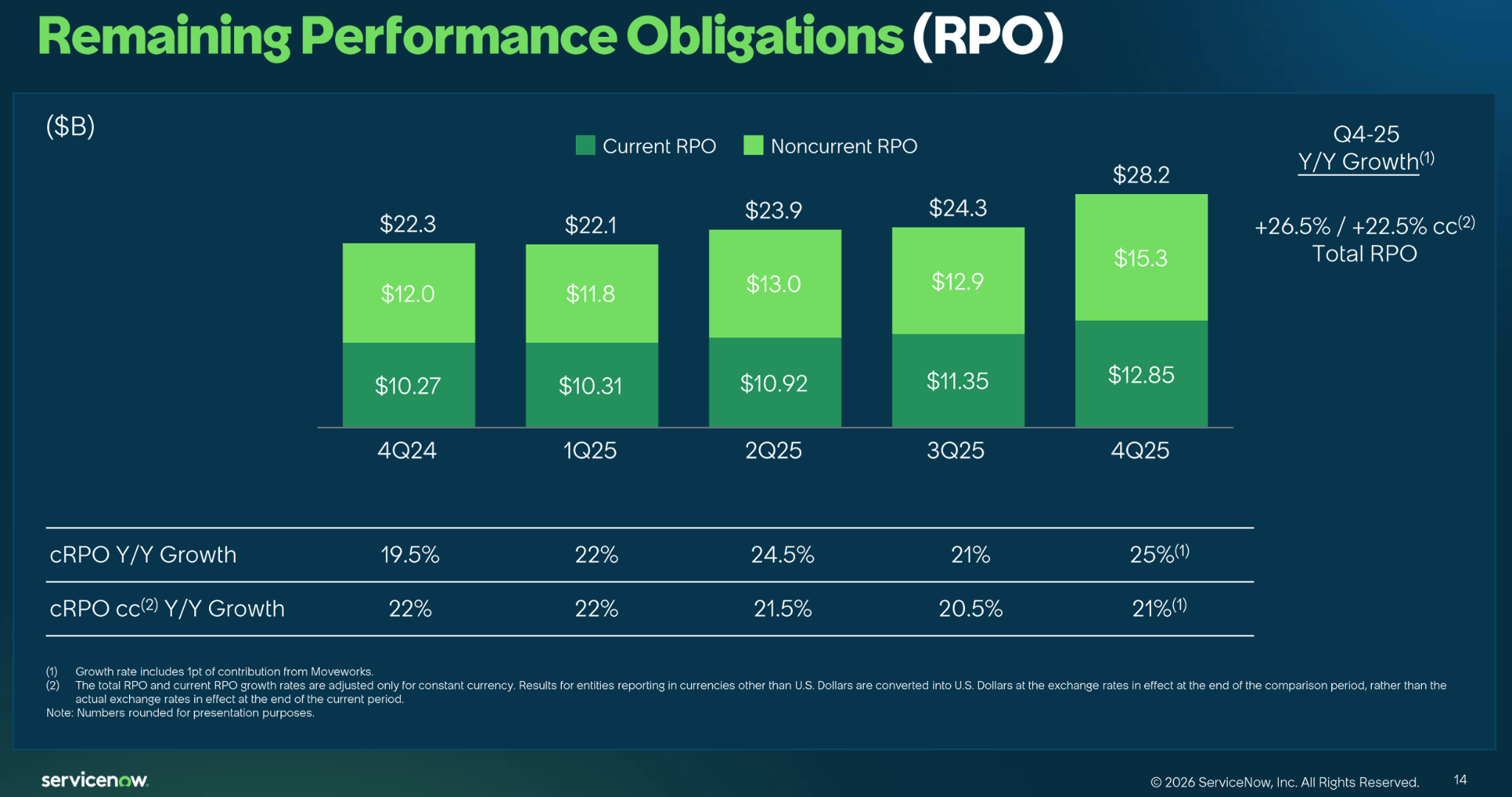

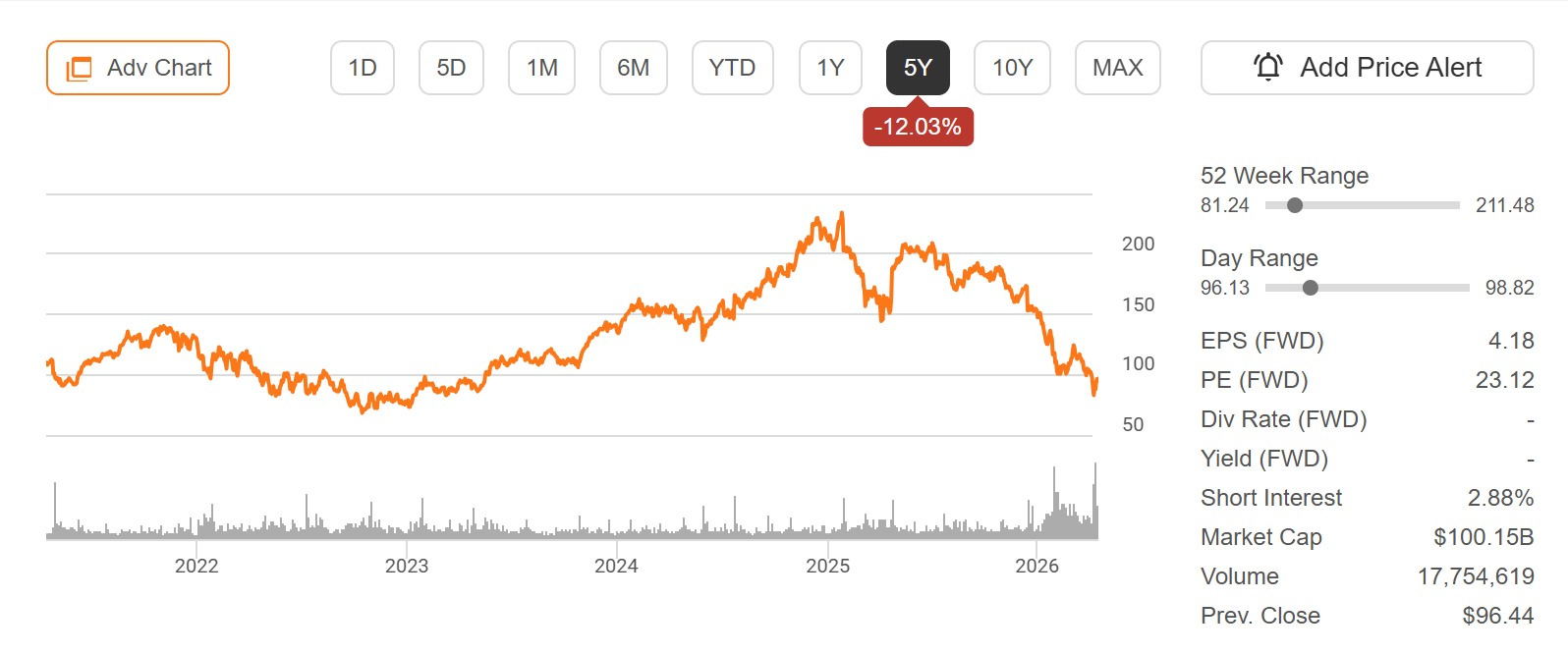

ServiceNow (NOW)

ServiceNow (-35.8% YTD) heads into the print at a critical moment, with shares under pressure amid broader concerns that AI could disrupt traditional SaaS models. Despite the selloff, underlying fundamentals remain strong – ServiceNow continues to deliver ~20%+ revenue growth and expanding deal sizes, while guiding for ~$15.5B in 2026 subscription revenue.

The debate now centers on whether AI is a tailwind or a threat. On one hand, ServiceNow is positioning itself as the “control layer” for enterprise AI workflows. On the other, investor concerns around AI agents replacing traditional software workflows have driven a sharp re-rating across the stock, with shares down materially over the past year.

Management has pushed back on that narrative, emphasizing platform integration and long-term demand strength. I’ll be watching: commentary on AI monetization, renewal trends, and whether ServiceNow can maintain pricing power in a shifting enterprise software landscape.

“We significantly beat expectations and issued exceptional guidance for 2026.”

ServiceNow, Inc. (NOW) Stock Performance, 5-Year Chart, Seeking Alpha

Tesla (TSLA)

Tesla (-10.9% YTD) reports Q1 earnings this week, with investors focused on whether the company can stabilize growth and margins amid intensifying competition and ongoing price adjustments.

Tesla has faced a more challenging operating environment in recent quarters, with vehicle deliveries under pressure, pricing cuts weighing on margins, and rising competition from both legacy automakers and Chinese EV players. At the same time, the company continues to position itself as more than just an automaker, leaning into AI, autonomy, and energy as key long-term drivers.

Last quarter, Tesla delivered softer-than-expected margins as aggressive pricing strategies weighed on profitability, even as revenue remained supported by volume growth.

Heading into this release, I’ll be watching for vehicle delivery trends, gross margin progression, and any updates on Full Self-Driving (FSD), AI initiatives, and the energy business. Commentary around demand elasticity and pricing strategy will also be critical as the company navigates a more competitive EV landscape.

“We continue to focus on cost efficiency and scaling production while navigating a dynamic demand environment.”

Tesla, Inc. (TSLA) Stock Performance, 5-Year Chart, Seeking Alpha

Investor Events / Global Affairs:

Adobe Summit is in focus after a sharp software selloff, Google Cloud Next will spotlight AI and enterprise momentum, and U.S.–Iran talks are in focus as ceasefire risks rise.

Adobe Summit 2026

Source: WorkFlowMAX

The three-day Adobe Summit kicks off this week, with Adobe expected to unveil major product updates and outline its strategy as competition in AI-driven creative tools intensifies.

The event comes at a critical moment for the stock following a sharp selloff (-30% YTD) across software, with Adobe under particular pressure as investors reassess its positioning in a rapidly evolving AI landscape. Recent product releases from competitors – like Claude design – have raised questions about how defensible Adobe’s pricing power and ecosystem will be as generative AI lowers barriers to content creation.

Adobe, Inc. (ADBE) Stock Performance, 5-Year Chart, Seeking Alpha

I’ll be watching how Adobe is integrating AI across its platform, monetizing tools like Firefly, and reinforcing its value proposition to both enterprise and individual users.

“Adobe is extending its commitment to an open ecosystem and expanding partnerships with Amazon Web Services (AWS), Anthropic, Google Cloud, IBM, Microsoft, NVIDIA and OpenAI, with deep interoperability for agentic orchestration across Adobe and third-party platforms.”

Google Cloud Next to Spotlight AI and Enterprise Momentum

The three-day Google Cloud Next kicks off in Las Vegas this week, with Google expected to showcase its latest advancements in generative AI, cloud infrastructure, and cybersecurity.

The event will focus heavily on practical product updates and developer tools, as Google looks to strengthen its position in the enterprise AI race against competitors like Microsoft and Amazon. Investors will be watching closely for updates on AI integration across Google Cloud, new partnerships, and signs of accelerating adoption from enterprise customers.

Google, Inc. (GOOG) Stock Performance, 5-Year Chart, Seeking Alpha

“The company hasn't revealed much about the upcoming event, but they promise to "explore the AI and cloud technology... making new opportunities possible." So, you can expect a focus on how Google plans to turn once-impossible ideas into practical tools.”

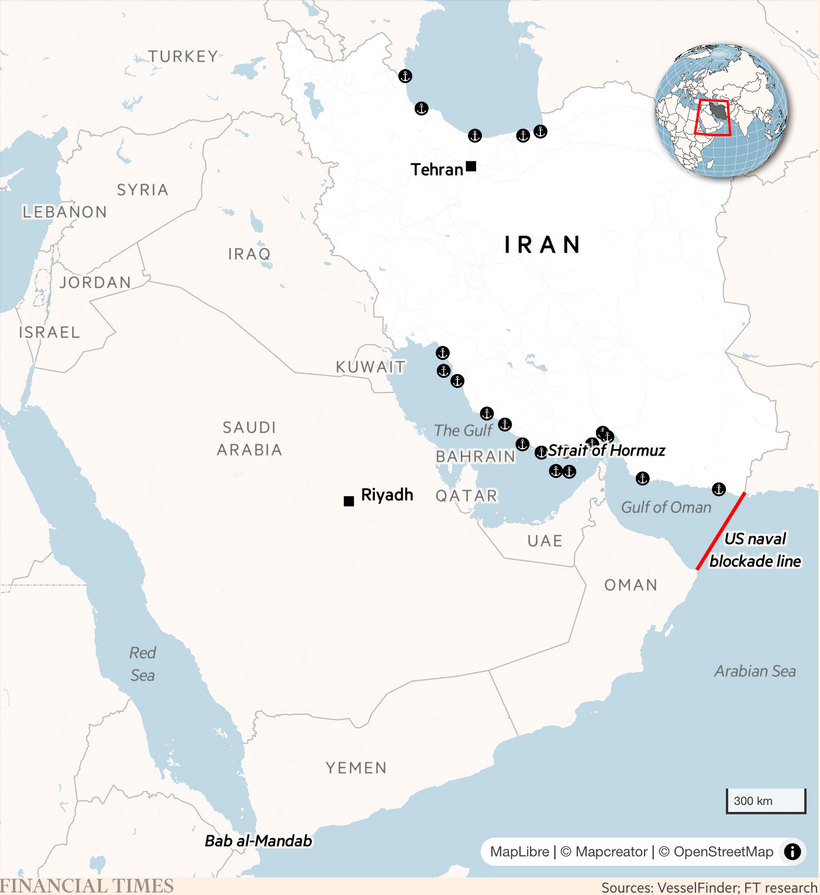

U.S.–Iran Talks in Focus as Ceasefire Risks Rise

Markets will be closely watching geopolitical developments this week as Donald Trump confirmed that U.S. negotiators are set to meet in Pakistan for potential peace talks with Iran, even as tensions continue to escalate across the region.

The talks come at a fragile moment, with the current ceasefire set to expire midweek and both sides signaling a willingness to resume conflict if negotiations break down. Iranian officials have indicated that progress has been made but emphasized that a final agreement remains distant, while also warning they are prepared to reengage militarily if terms are not met.

A key sticking point remains control over the Strait of Hormuz, where Iran has threatened to again restrict shipping unless U.S. demands – including the lifting of port blockades – are addressed. At the same time, U.S. forces are reportedly preparing to intercept and seize Iran-linked oil shipments, further raising the risk of escalation.

For investors, the situation underscores a highly fluid geopolitical backdrop, where diplomacy and military posturing are unfolding simultaneously. The outcome of this week’s talks could have immediate implications for oil prices, global shipping flows, and broader market risk sentiment, particularly if the ceasefire collapses or tensions expand further.

This is long but worth the read! —

“If there are questions over whether this weeks peace talks will go ahead, Pakistan may well have the answer. The government, which is mediating the negotiations, has already imposed a strict security bubble ready for the arrival of Vice President JD Vance and the Iranian delegation. Whole highways are closed, with police telling NBC News they began stopping traffic at midnight. Hotels have been emptied out in preparation for the sensitive meetings.

The reality is that even the furious Iranian insistence that it hasn’t decided whether to come is part of the negotiations, trying to put the American side on the back foot. Further complicating the picture, different Iranian leaders are sending contradictory messages. The IRGC vowed revenge for the seizing of an Iranian cargo ship yesterday, even as Iranian President Masoud Pezeshkian continued to emphasize diplomacy. All of this makes it very hard for the two sides to reach a deal within days. The Turkish Foreign Minister Hakan Fidan told me over the weekend that the ceasefire deadline will have to be extended.”

Major Economic Events:

A look into consumer sentiment and retail sales.

Monday (4/20): N/A

Tuesday (4/21): Business inventories, Pending home sales, Retail sales, Retail sales ex-autos

Wednesday (4/22): N/A

Thursday (4/23): Initial jobless claims, S&P flash manufacturing PMI, S&P flash services PMI

Friday (4/24): Consumer sentiment (final)

What We’re Watching:

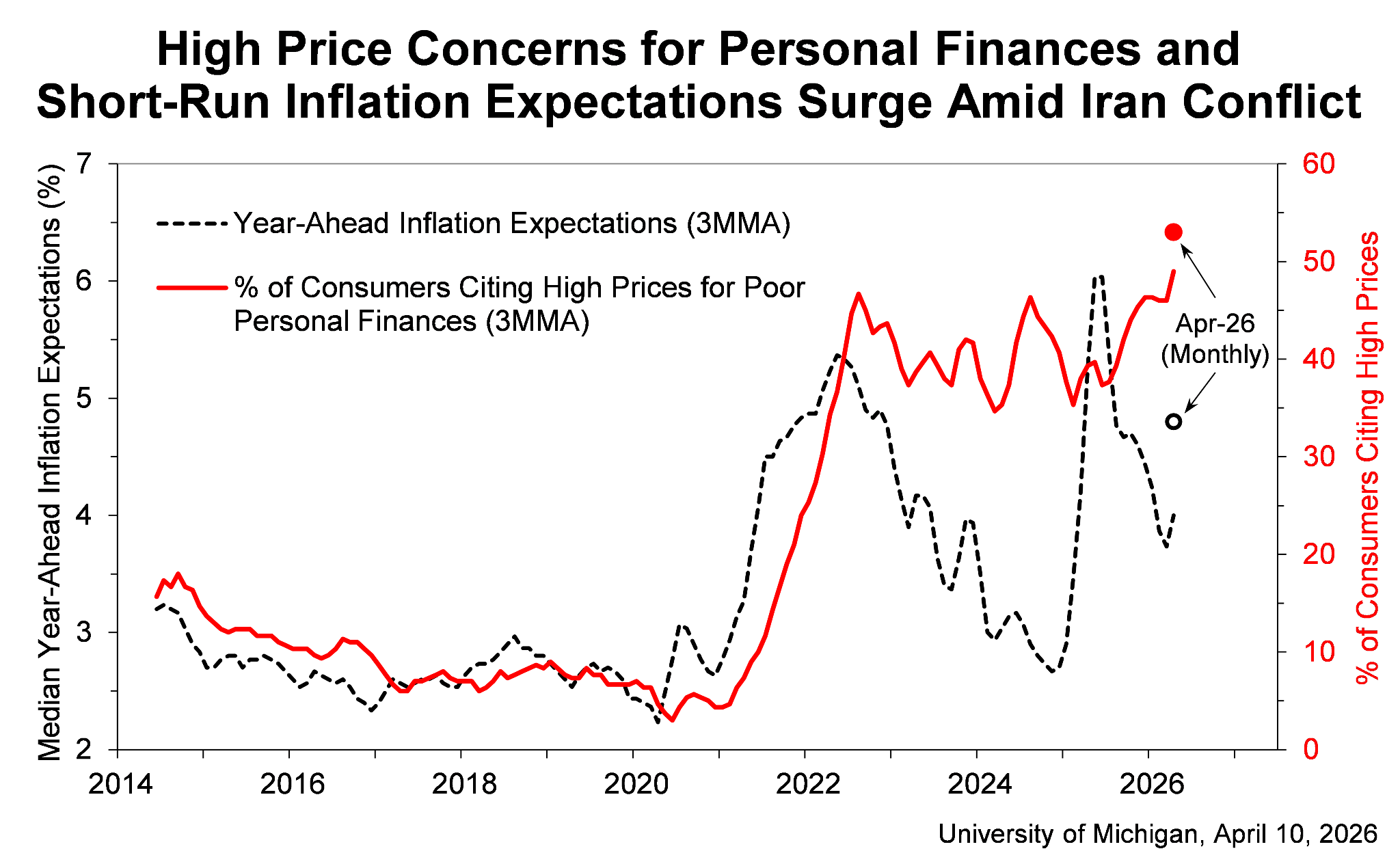

Michigan Consumer Sentiment

The University of Michigan Consumer Sentiment Index plunged to 47.6 in early April, marking an 11% drop from March and one of the weakest readings on record, as geopolitical tensions and rising costs weighed heavily on consumer confidence.

The decline was broad-based across all demographics and survey components, with expectations for business conditions falling 20% and personal financial outlooks dropping 11%. Consumers pointed to higher prices and declining asset values as key concerns, while buying conditions for big-ticket items like vehicles and durable goods deteriorated further.

Inflation expectations also moved sharply higher. Year-ahead expectations jumped to 4.8% from 3.8%, the largest monthly increase in nearly a year, while long-term expectations rose to 3.4%.

Economists expect the following this week:

Consumer Sentiment: 47.6 vs. 53.5 prior

1-Year Inflation Expectations: 4.8% vs. 3.8% prior

5-Year Inflation Expectations: 3.4% vs. 3.2% prior

“Consumers are increasingly concerned about both rising prices and the broader economic outlook, particularly amid geopolitical uncertainty.”

Retail Sales

U.S. retail sales rose 0.6% MoM in February, rebounding from a 0.1% decline in January and coming in above expectations of 0.5%, marking the strongest monthly gain in seven months.

The strength was broad-based, with notable increases across discretionary categories including department stores (+3%), health and personal care (+2.3%), and clothing (+2%), alongside solid gains in autos and general merchandise. Online sales and gasoline spending also moved higher, pointing to steady demand across both goods and services.

While some softness remained in food and beverage and furniture sales (-1% each), the overall trend suggests consumers are continuing to spend despite mixed sentiment data and ongoing geopolitical uncertainty. Importantly, core retail sales – which feed directly into GDP – rose 0.5%, exceeding expectations and signaling solid underlying consumption.

Economists expect the following this week:

Retail Sales (MoM): +0.6% vs. -0.1% prior

Core Retail Sales: +0.5% vs. +0.3% expected

“Retail sales grew…in March as the first wave of tax refunds offset higher gas prices resulting from the conflict in the Middle East. Despite record-low consumer sentiment and the highest inflation rate in two years, consumers continued to spend on household priorities.”

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

This content is sponsored by NEOS Investments. The creator is compensated by NEOS to discuss NEOS ETFs. This content is for informational purposes only, and is not personalized investment, tax, or legal advice, and does not constitute an offer to buy or sell any security. Investing involves risk, including possible loss of principal. Before investing, carefully review the NEOS ETFs prospectus at neosfunds.com.

Grit is a publisher of financial information, not an investment advisor. Grit does not provide personalized or individualized investment advice or information that is tailored to the needs of any particular recipient. Grit does not guarantee the accuracy or completeness of the information provided in this page. All statements and expressions herein are the sole opinion of the author or paid advertiser.

Cover Image Source: WorkFlowMAX

THE INFORMATION CONTAINED ON THIS WEBSITE IS NOT AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE, AND DOES NOT PURPORT TO BE AND DOES NOT EXPRESS ANY OPINION AS TO THE PRICE AT WHICH THE SECURITIES OF ANY COMPANY MAY TRADE AT ANY TIME. THE INFORMATION AND OPINIONS PROVIDED HEREIN SHOULD NOT BE TAKEN AS SPECIFIC ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. INVESTORS SHOULD MAKE THEIR OWN INVESTIGATION AND DECISIONS REGARDING THE PROSPECTS OF ANY COMPANY DISCUSSED HEREIN BASED ON SUCH INVESTORS’ OWN REVIEW OF PUBLICLY AVAILABLE INFORMATION AND SHOULD NOT RELY ON THE INFORMATION CONTAINED HEREIN. INVESTORS SHOULD OBTAIN INDIVIDUAL INVESTMENT ADVICE BASED ON THEIR OWN CIRCUMSTANCES BEFORE MAKING AN INVESTMENT DECISION

No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned.

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Any projections, market outlooks or estimates herein are forward looking statements and are inherently unreliable. They are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities discussed herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and Grit undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional material.

Grit does not accept any liability whatsoever for any direct or consequential loss, however arising, directly or indirectly, from any use of the information contained herein.

By using the Site or any related social media account, you are indicating your consent and agreement to this disclaimer and our terms of use. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Please read: Terms of Use, Privacy Policy, Disclosure Policy and Disclaimer Policy

If you have any questions please contact us at [email protected]