- GRIT

- Posts

- 👉 Roller Coaster of War Updates

👉 Roller Coaster of War Updates

Carnival Cruises, Consumer Sentiment, De-escalation

Austin Hankwitz

23 Mar

Together with WisdomTree

Welcome to your new week.

During crazy times like these in the market, it’s best to stay well-informed. If you want full access to our Week in Review editions, monthly livestreams , portfolio access, monthly stock deep dives, and more — consider upgrading your subscription.

Let’s dive right in.

Position Portfolios for Structural Defense Growth

Geopolitical uncertainty is rising and global defense spending is accelerating alongside it. A multi-year modernization cycle is underway, reshaping the investment landscape beyond short-term headlines.

WisdomTree’s Defense Suite of ETFs provides targeted, globally diversified exposure to companies supporting today’s evolving security needs—from advanced technologies to next-generation defense systems.

Key Earnings Announcements:

Earnings reports officially move away from the spotlight this week, but some notable names like Carnival Corporation will be sharing their results.

Monday (3/23): AGI, BioLineRx, Lithium Argentina, WeRide

Tuesday (3/24): Braze, Core & Main, Sanara MedTech, AAR Corp

Wednesday (3/25): Beyond Meat, Chewy, Cintas, Enerpac Tool Group, Paychex

Thursday (3/26): Blink Charging, Lovesac, Lucid Group, Veritone

Friday (3/27): Carnival, Autolus, Oxford Industries, Argan

What We’re Watching:

Carnival Corporation (CCL)

Carnival Corporation (-21% YTD) reports Q1 FY2026 earnings this week, with investors focused on whether strong travel demand and pricing momentum can continue to offset elevated costs and a still-leveraged balance sheet.

Carnival has been one of the biggest beneficiaries of the post-pandemic travel rebound, with record bookings, higher ticket prices, and strong onboard spending driving a sharp recovery in revenue. Last quarter, the company delivered solid results with improved occupancy and yield, alongside continued progress on deleveraging.

Heading into this print, we’ll be watching:

Booking trends and forward demand commentary

Ticket pricing and onboard spending (yield growth)

Fuel and operating cost pressures

Debt reduction and balance sheet progress

“Demand for our cruise brands remains incredibly strong, with customers prioritizing experiences.”

Carnival Corporation & plc. (CCL) Stock Performance, 5-Year Chart, Seeking Alpha

Investor Events / Global Affairs:

There’s been a 24-hour roller coaster of escalation and de-escalation regarding the Middle East, and the ShopTalk Conference kicks off in Las Vegas.

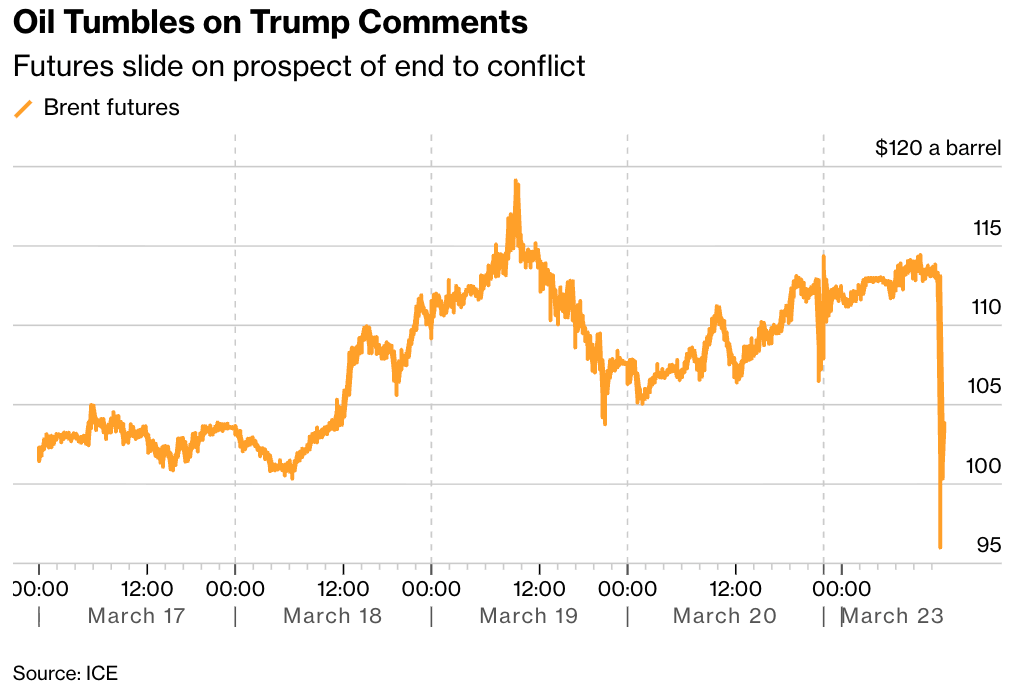

Middle East Escalation and Now De-escalation?

Sources: Evelyn Hockstein | Reuters

President Donald Trump signaled a potential pivot toward de-escalation, saying the U.S. is “very intent on making a deal” with Iran and ordering a five-day pause on planned strikes targeting energy infrastructure. He described recent interactions as “productive,” suggesting a diplomatic off-ramp may be emerging after weeks of escalating conflict.

However, Iranian officials quickly pushed back, denying that any direct or indirect negotiations have taken place. This disconnect highlights how fragile the situation remains, with both sides sending mixed signals while tensions stay elevated. The Strait of Hormuz — a critical chokepoint for roughly 20% of global oil supply — remains largely disrupted, keeping pressure on global energy markets.

Markets reacted positively to the potential for diplomacy. Oil prices pulled back, the U.S. dollar weakened, and equity futures rallied as investors priced in a reduced risk of further escalation. The move underscores how sensitive markets are to headlines, with geopolitical developments now driving short-term price action.

The bigger picture is still uncertain. If talks materialize, it could ease inflation pressures tied to energy and stabilize global markets. But if negotiations fail or escalation resumes, oil and volatility could quickly spike again — making this one of the most important macro storylines to watch right now.

“I am pleased to report that the United States of America, and the country of Iran, have had, over the last two days, very good and productive conversations regarding a complete and total resolution of our hostilities in the Middle East. Based on the tenor and tone of these in-depth, detailed, and constructive conversations, which will continue throughout the week, I have instructed the Department of War to postpone any and all military strikes against Iranian power plants and energy infrastructure for a five-day period, subject to the success of the ongoing meetings and discussions. Thank you for your attention to this matter!”

ShopTalk Spring 2026

The annual ShopTalk Conference kicks off in Las Vegas this week, bringing together executives across retail, e-commerce, and consumer brands to discuss the evolving landscape of digital commerce and customer engagement.

A keynote from Steve Huffman of Reddit will highlight the growing intersection of social platforms and commerce, while leadership teams from Wayfair, Stitch Fix, Pinterest, Gap Inc., Dutch Bros, and SharkNinja are also set to present.

Investors will be watching for commentary on consumer demand trends, digital advertising, AI-driven personalization, and e-commerce profitability, particularly as brands navigate a more selective and price-sensitive consumer environment.

“Retail leaders are looking for actionable insights and meaningful partnerships that will help them navigate new opportunities. With AI as the backdrop for everything happening in retail, we’ll look at AI driven developments as well as the opportunities for more human-centered experiences.

Those interested in the AI revolution can take advantage of a fresh new comprehensive program designed to help guide retail decision-makers by providing discussions, case studies and best practices in implementing AI initiatives.”

Major Economic Events:

Fedspeak, initial jobless claims and Michigan’s consumer sentiment survey highlight the week.

Monday (3/23): Construction spending

Tuesday (3/24): Fed Gov. Michael Barr speaks, S&P flash manufacturing PMI, S&P flash services PMI, U.S. productivity (revision)

Wednesday (3/25): Fed Gov. Stephen Miran speaks, Import price index, Import price index ex-fuel

Thursday (3/26): Fed Gov. Lisa Cook speaks, Fed Gov. Michael Barr speaks, Fed Gov. Stephen Miran speaks, Fed Vice Chair Philip Jefferson speaks, Initial jobless claims

Friday (3/27): Consumer sentiment (final)

What We’re Watching:

Consumer Sentiment

The University of Michigan Consumer Sentiment Index fell to 55.5 in March, down from 56.6 in February and marking the lowest level in three months, as rising geopolitical tensions and higher gasoline prices pressured household confidence.

The decline was broad-based, with consumers across income levels, age groups, and political affiliations reporting weaker expectations for their personal finances, which dropped 7.5% nationwide. The deterioration follows the onset of the U.S.–Iran conflict, with energy costs emerging as the most immediate concern for consumers.

Inflation expectations showed a mixed picture. Year-ahead expectations held at 3.4%, snapping a six-month streak of declines, while long-term expectations edged down slightly to 3.2%.

Economists expect the following this week:

Consumer Sentiment: 55.5 vs. 56.6 prior

1-Year Inflation Expectations: 3.4% vs. 3.4% prior

5-Year Inflation Expectations: 3.2% vs. 3.3% prior

“Consumers are clearly reacting to higher energy prices and geopolitical uncertainty, which is weighing on confidence even as longer-term inflation expectations remain stable.”

Initial Jobless Claims

Initial jobless claims fell by 8,000 to 205,000 in the second week of March, coming in well below expectations and signaling that layoffs remain subdued despite mixed signals from recent labor data.

Continuing claims edged up slightly to 1.86 million, but remain on a downward trend since late last year, suggesting that while hiring may be slowing, displaced workers are not facing a sharp deterioration in reemployment conditions.

The data contrasts with softer readings in recent payroll reports, reinforcing the view that the labor market is cooling gradually rather than weakening outright. Claims from federal employees – closely watched amid government shutdown concerns – rose modestly to 643.

Economists expect the following this week:

Initial Jobless Claims: 205K vs. 213K prior

Continuing Claims: 1.86M vs. 1.85M prior

“Layoffs remain historically low –the labor market is slowing, but not breaking.”

WisdomTree Disclosures: Investors should carefully consider the investment objectives, risks, charges and expenses of the Fund before investing. For a prospectus or, if available, the summary prospectus containing this and other important information about the fund, call 866.909.9473 or visit WisdomTree.com/investments. Read the prospectus or, if available, the summary prospectus carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S.

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

This content is sponsored by NEOS Investments. The creator is compensated by NEOS to discuss NEOS ETFs. This content is for informational purposes only, and is not personalized investment, tax, or legal advice, and does not constitute an offer to buy or sell any security. Investing involves risk, including possible loss of principal. Before investing, carefully review the NEOS ETFs prospectus at neosfunds.com.

Grit is a publisher of financial information, not an investment advisor. Grit does not provide personalized or individualized investment advice or information that is tailored to the needs of any particular recipient. Grit does not guarantee the accuracy or completeness of the information provided in this page. All statements and expressions herein are the sole opinion of the author or paid advertiser.

Cover Image Source: Evelyn Hockstein | Reuters

THE INFORMATION CONTAINED ON THIS WEBSITE IS NOT AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE, AND DOES NOT PURPORT TO BE AND DOES NOT EXPRESS ANY OPINION AS TO THE PRICE AT WHICH THE SECURITIES OF ANY COMPANY MAY TRADE AT ANY TIME. THE INFORMATION AND OPINIONS PROVIDED HEREIN SHOULD NOT BE TAKEN AS SPECIFIC ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. INVESTORS SHOULD MAKE THEIR OWN INVESTIGATION AND DECISIONS REGARDING THE PROSPECTS OF ANY COMPANY DISCUSSED HEREIN BASED ON SUCH INVESTORS’ OWN REVIEW OF PUBLICLY AVAILABLE INFORMATION AND SHOULD NOT RELY ON THE INFORMATION CONTAINED HEREIN. INVESTORS SHOULD OBTAIN INDIVIDUAL INVESTMENT ADVICE BASED ON THEIR OWN CIRCUMSTANCES BEFORE MAKING AN INVESTMENT DECISION

No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned.

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Any projections, market outlooks or estimates herein are forward looking statements and are inherently unreliable. They are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities discussed herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and Grit undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional material.

Grit does not accept any liability whatsoever for any direct or consequential loss, however arising, directly or indirectly, from any use of the information contained herein.

By using the Site or any related social media account, you are indicating your consent and agreement to this disclaimer and our terms of use. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Please read: Terms of Use, Privacy Policy, Disclosure Policy and Disclaimer Policy

If you have any questions please contact us at [email protected]