- GRIT

- Posts

- 👉 Springtime Earnings Roll On

Together with Your Best Credit Cards

Welcome to your new week.

Consider checking out a huge 100,000 point offer on one of our favorite travel rewards credit cards. This is the best of the year on this card and it likely will be expiring within the next few days!

Key Earnings Announcements:

AMD, Ford, Hims, Palantir, and Walt Disney highlight this week of mixed earnings.

Monday (5/5): Ford, Hims & Hers, Onsemi, Palantir, Realty Income, Tyson Foods

Tuesday (5/6): AMD, Arista Networks, Celsius, Constellation Energy, Datadog, Energy Transfer, Ferrari, Lucid, Rivian, Supermicro, Tempus, Wynn Resorts

Wednesday (5/7): Applovin, Arm, Barrick Gold, Carvana, Doordash, Novo Nordisk, Oscar Health, Teva, Uber, Unity Software, Vistra Energy, Walt Disney

Thursday (5/8): Cloudflare, Coinbase, ConocoPhillips, Crocs, D-Wave, DraftKings, Marathon Digital, MercadoLibre, Peloton, Shopify, SoundHound, Warner Bros

Friday (5/9): Enbridge, Terawulf

What We’re Watching:

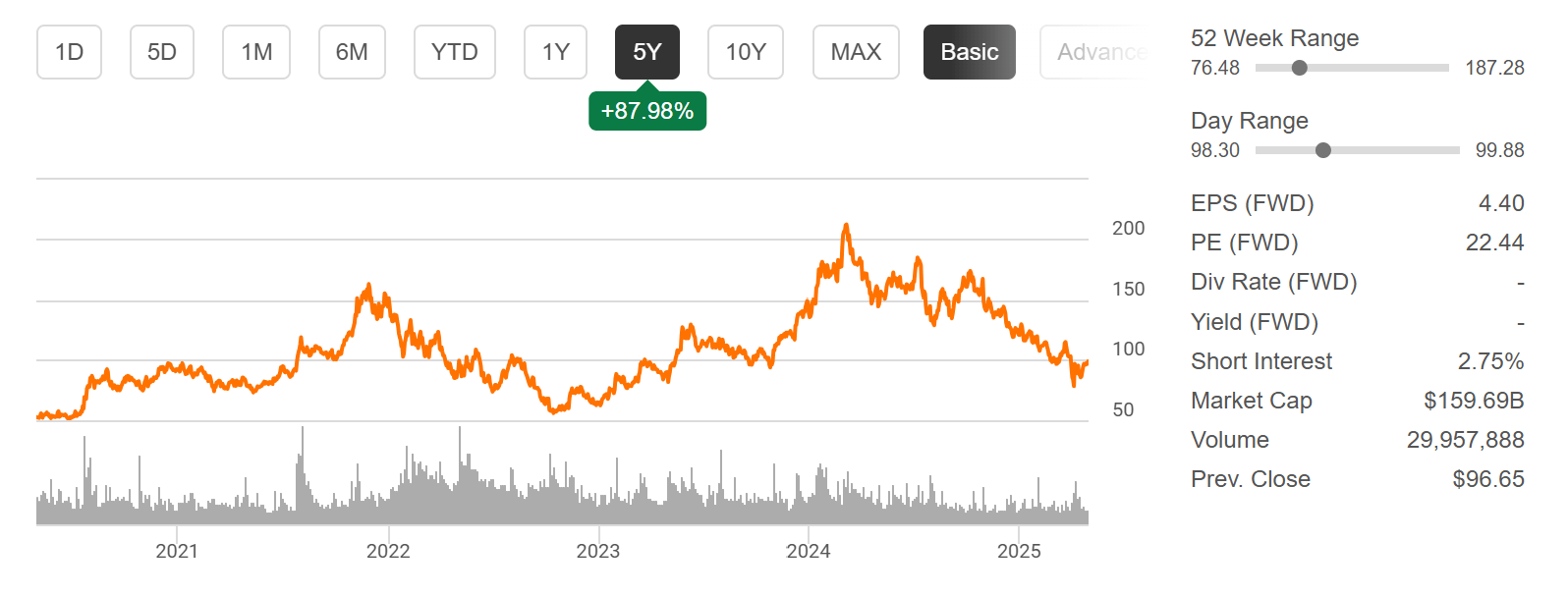

Advanced Micro Devices (AMD)

Advanced Micro Devices reports Tuesday, down -20% YTD despite a +30% recovery from April lows. Q4 2024’s revenue came back as $7.6B — up +24% YoY — driven by a record $3.9B data center segment. The data center business, which comprises 49% of revenue, faces CapEx cut risks — while a $800M charge looms from U.S. export fees on China AI chips.

Data center growth — up +69% YoY in Q4 — could falter if hyperscalers cut CapEx amid global economic uncertainty and trade wars. But a forward EBITDA multiple of 21.2x signals potential undervaluation, and Meta’s CapEx hike supports AI chip demand. I am very interested in hearing CEO Lisa Su’s AI guidance. She’s had a bad habit of underdelivering during earnings reports, leaving investors frustrated. I recently shared this as a stock that seems undervalued and that I’m interested in buying — so I will be tuning in!

“AMD’s exposure to Taiwanese and Chinese suppliers may lead to higher input costs and business disruptions.”

Advanced Micro Devices, Inc. (AMD) Stock Performance, 5-Year Chart, Seeking Alpha

Ford (F)

Source: Ford Investor Deck

Ford reports earnings Monday after the bell. Shares are up +3% YTD after posting record 2024 revenue of $185B and adjusted EBIT of $10.2B. Ford Pro led the way with a 13.5% EBIT margin, driven by commercial vehicle demand, software, and physical services — now contributing 13% of Pro’s total EBIT. The company delivered $6.7B in free cash flow with a 65% cash conversion rate, exceeding targets, and announced both a regular and supplemental Q1 dividend.

While Ford remains America’s #1 ICE brand and #2 in EVs, EV losses continue to weigh on sentiment. Model e posted a -$1.3B operating loss in Q1 as sales fell -16% YoY. By contrast, hybrids grew +42%, underscoring Ford’s pivot toward more profitable segments. I’ll be listening for tariff impacts, cost updates, and important future guidance. While I’m not a Ford shareholder, this auto giant employs nearly 100K Americans and we’ll be watching how they are doing.

“Let’s be real honest, long term, a 25% tariff across the Mexico and Canadian border would blow a hole in the U.S. industry that we have never seen.”

Ford Motor Company (F) Stock Performance, 5-Year Chart, Seeking Alpha

Investor Events / Global Affairs:

Crude oil’s price is dropping amid the OPEC+ meeting, addressing the ole “Sell in May” adage, Japan has become increasingly important in the trade wars, and the NAMA Show in Las Vegas could provide insight into consumer spending / preferences.

Crude Oil Dropping

Source: euronews.com

Crude prices dropped over -3% Monday after OPEC+ moved up its originally scheduled Monday meeting to Saturday, where it announced a faster unwinding of production cuts — adding +411K Barrels Per Day (BPD) in June and raising concerns about oversupply. The bloc has now reversed 44% of its prior cuts, with pressure from Saudi Arabia to penalize non-compliant members like Iraq and Kazakhstan. Barclays slashed its Brent forecast, while renewed Middle East tensions added geopolitical risk to an already volatile market.

Trump added to the tensions on Truth Social over the weekend, where he wrote, “All purchases of Iranian Oil, or Petrochemical products, must stop, NOW!” He emphasized that those who continue to buy Iranian oil will not be able to conduct business with the U.S. “in any way, shape, or form.” This move is part of his "maximum pressure" campaign against Iran, aimed at curbing its oil exports and influencing its nuclear program negotiations. The statement particularly escalates tensions with China, Iran’s largest oil customer, which imported nearly 90% of Iran’s crude oil exports in 2023.

Let’s keep an eye on the oil market as the week proceeds.

“The prospects of an oversupplied oil market, rising tariffs, uncertainty in Mexico and activity weakness in Saudi Arabia are collectively constraining international upstream spending levels.”

Sell in May and Go Away?

As May kicks off, the old adage is back — but we’re not convinced that year’s policy-driven, volatile market will follow seasonal trends. While data shows weaker average returns from May to October — it’s hard to imagine that monetary policy, tariffs, and geopolitics won’t play a bigger role in shaping market direction. With the S&P 500 notching its longest win streak since 2004 with nine green days in a row — this summer may be more about headlines than historical references.

If you are really focused on historical data (which I don’t necessarily recommend when making an investment thesis) — the first May after presidential elections is generally strong:

One thing is for certain — I’m not going to be “selling in May” and instead I’m going to be deploying ~$30K into my portfolio throughout the month. I still believe we have some choppiness ahead of us, but if we’re lucky enough to get a “De-escalation Day” — this market is going to rip on a moment’s notice.

"Seasonality data can provide important insights into the potential market climate, but it doesn't represent the current weather."

Japan Trade Talks Enter the Spotlight

Japan’s Chief Negotiator Ryosei Akazawa in Washington, DC, on May 1. Source: Stefani Reynolds / Bloomberg

Japan hopes to finalize a trade agreement with the U.S. by June, though key disagreements remain, particularly over Washington's 25% tariffs on Japanese car exports. Chief negotiator Ryosei Akazawa held extensive talks with top U.S. officials, including Treasury Secretary Scott Bessent, but no breakthrough was announced. Japan is pushing for a comprehensive deal that also addresses non-tariff barriers and increases U.S. agricultural imports, while the U.S. wants to maintain its tariff framework.

Finance Minister Katsunobu Kato hinted that Japan’s large holdings of U.S. Treasuries could be used as leverage, though it’s unclear how seriously this is being considered. With auto exports and agriculture critical to Japan’s economy and national elections looming, the government is emphasizing that any deal must protect its national interests.

In response to headlines that Japan will be dumping U.S. Treasuries…

"My comments were made in response to a question whether Japan could, as a bargaining tool in trade negotiations, explicitly reassure Washington it wouldn't sell its Treasury holdings easily.”

NAMA Show

Source: NAMA Show

The National Automatic Merchandising Association (NAMA) Show 2025 kicks off this Wednesday, May 7, at the Las Vegas Convention Center — bringing together leaders in vending, micro markets, and unattended retail. Attendees will experience the latest in smart kiosks, AI-powered vending, and contactless payment systems.

Industry giants like PepsiCo, Coca-Cola, Hershey, and Nayax will showcase cutting-edge solutions, while VenHub unveils its fully autonomous smart store. The event runs through Friday, May 9, offering a glimpse into the future of convenience services and how consumer spending is changing for some of the largest snack and beverage companies in the world.

You can learn more here, and we’ll report back if any noteworthy news comes out of the event.

Major Economic Events:

Tariffs are in focus as the Fed reveals their next interest rate decision, and the US Trade Deficit comes to light.

Source: Reuters / Carlos Barria / File Photo

Monday (5/5): ISM Services, S&P Final U.S. Services PMI

Tuesday (5/6): U.S. Trade Deficit

Wednesday (5/7): Consumer Credit, Fed Chair Powell Press Conference, FOMC Meeting

Thursday (5/8): Initial Jobless Claims, U.S. Productivity, Wholesale Inventories

Friday (5/9): Fed Gov Adriana Kugler Speaks, Fed Governor Christopher Waller and New York Fed President John Williams on Panel, Fed Gov Lisa Cook Speaks, Fed Gov Michael Barr Speaks, New York Fed President John Williams Speaks

What We’re Watching:

FOMC Meeting & Powell Press Conference

The Fed held interest rates steady at 4.25%-4.5% in March, extending its pause on cuts amid growing concerns that inflation could stay elevated longer than expected — especially with tariffs pushing prices higher. While policymakers still project -50bps of cuts this year, they raised their inflation outlook for 2025-26 and trimmed their growth forecast, signaling a more cautious path ahead.

Source: CME FedWatch Tool

The odds of a rate cuts over the next three Fed meetings are below:

This week: 3.1% (shown above)

June: 31.8%

July: 77.7%

“A good part of the central bank's higher inflation expectation comes from tariffs. … If the economy remains strong, and inflation does not continue to move sustainably toward 2%, we can maintain policy restraint for longer. If the labor market were to weaken unexpectedly, or inflation were to fall more quickly than anticipated, we can ease policy accordingly”

U.S. Trade Deficit

The U.S. trade deficit shrank to -$122.7B in February, down from a record $130.7B in January, as exports jumped +2.9% on stronger gold and vehicle sales. Imports held near record highs at $401.1B, still elevated from tariff-driven frontloading. The goods gap narrowed, but the services surplus also dipped. Trade balances improved with China and Canada, but deficits widened with the EU, Mexico, and Vietnam — keeping global trade tensions in focus ahead of new tariff policy updates.

The trade deficit is expected to grow in this week’s report for March data — with a -$136B monthly deficit expected.

“Trump’s tariff rates and implementation aren’t perfect. Crude mercantilism shouldn’t be defended. And the academics are right when they say tariffs don’t necessarily help workers. Yet the MAGA movement is also right when its says chronic trade deficits underscore a fundamental problem with the U.S. economy. By realizing the true culprits are the Fed and Treasury, the Trump reformers have a chance at providing a genuine solution.”

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Disclosure: The author of this post has an existing business relationship with NEOS Investment Management, LLC, and is also a holder of numerous NEOS ETFs. The thoughts and opinions in this written piece are solely those of the author.

Grit is a publisher of financial information, not an investment advisor. Grit does not provide personalized or individualized investment advice or information that is tailored to the needs of any particular recipient. Grit does not guarantee the accuracy or completeness of the information provided in this page. All statements and expressions herein are the sole opinion of the author or paid advertiser.

THE INFORMATION CONTAINED ON THIS WEBSITE IS NOT AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE, AND DOES NOT PURPORT TO BE AND DOES NOT EXPRESS ANY OPINION AS TO THE PRICE AT WHICH THE SECURITIES OF ANY COMPANY MAY TRADE AT ANY TIME. THE INFORMATION AND OPINIONS PROVIDED HEREIN SHOULD NOT BE TAKEN AS SPECIFIC ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. INVESTORS SHOULD MAKE THEIR OWN INVESTIGATION AND DECISIONS REGARDING THE PROSPECTS OF ANY COMPANY DISCUSSED HEREIN BASED ON SUCH INVESTORS’ OWN REVIEW OF PUBLICLY AVAILABLE INFORMATION AND SHOULD NOT RELY ON THE INFORMATION CONTAINED HEREIN. INVESTORS SHOULD OBTAIN INDIVIDUAL INVESTMENT ADVICE BASED ON THEIR OWN CIRCUMSTANCES BEFORE MAKING AN INVESTMENT DECISION

No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned.

Cover image source: AMD

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Any projections, market outlooks or estimates herein are forward looking statements and are inherently unreliable. They are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities discussed herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and Grit undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional material.

Grit does not accept any liability whatsoever for any direct or consequential loss, however arising, directly or indirectly, from any use of the information contained herein.

By using the Site or any related social media account, you are indicating your consent and agreement to this disclaimer and our terms of use. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Please read: Terms of Use, Privacy Policy, Disclosure Policy and Disclaimer Policy

If you have any questions please contact us at [email protected]