- GRIT

- Posts

- 👉 USO +58% YTD (Wow)

Welcome to your new week.

During crazy times like these in the market, it’s best to stay well-informed. If you want full access to our Week in Review editions, monthly livestreams, portfolio access, monthly stock deep dives, and more — consider upgrading your subscription.

Congrats to those that ended up following along with some of my recent oil investing ideas — including IPI (+51% YTD) and USO (+58% YTD).

Read on for everything you need to watch over the coming days.

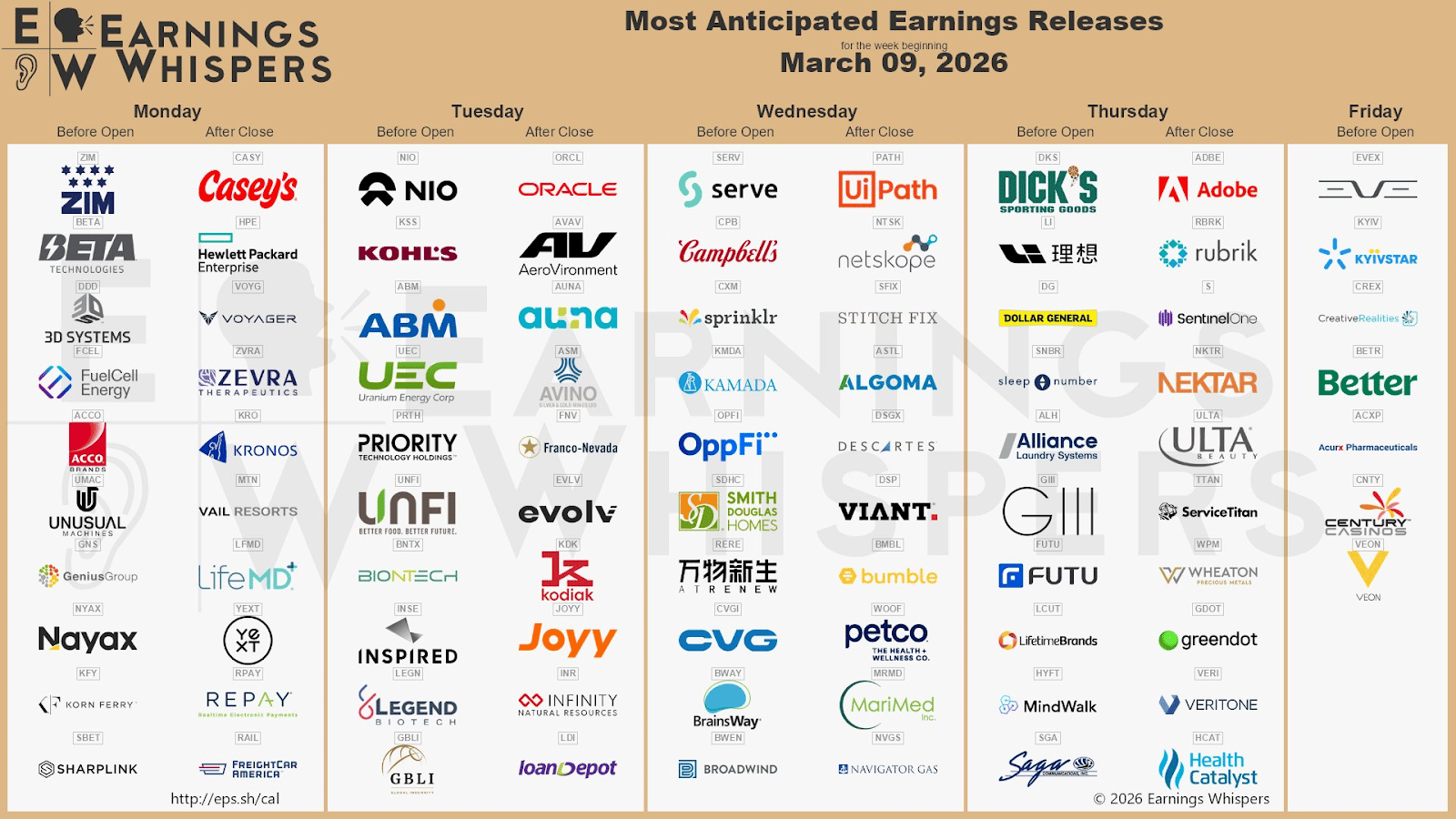

Key Earnings Announcements:

Adobe, Casey’s, Dick’s, Dollar General, and Oracle highlight the week

Monday (3/9): Casey’s, Hewlett Packard Enterprise, Vail Resorts, ZIM

Tuesday (3/10): ABM Industries, AeroVironment, BioNTech, Franco-Nevada, Kohl’s, NIO, Oracle

Wednesday (3/11): Campbell’s, Descartes Systems, Petco, UiPath

Thursday (3/12): Adobe, Dick’s Sporting Goods, Dollar General, SentinelOne, Ulta Beauty

Friday (3/13): VEON

What We’re Watching:

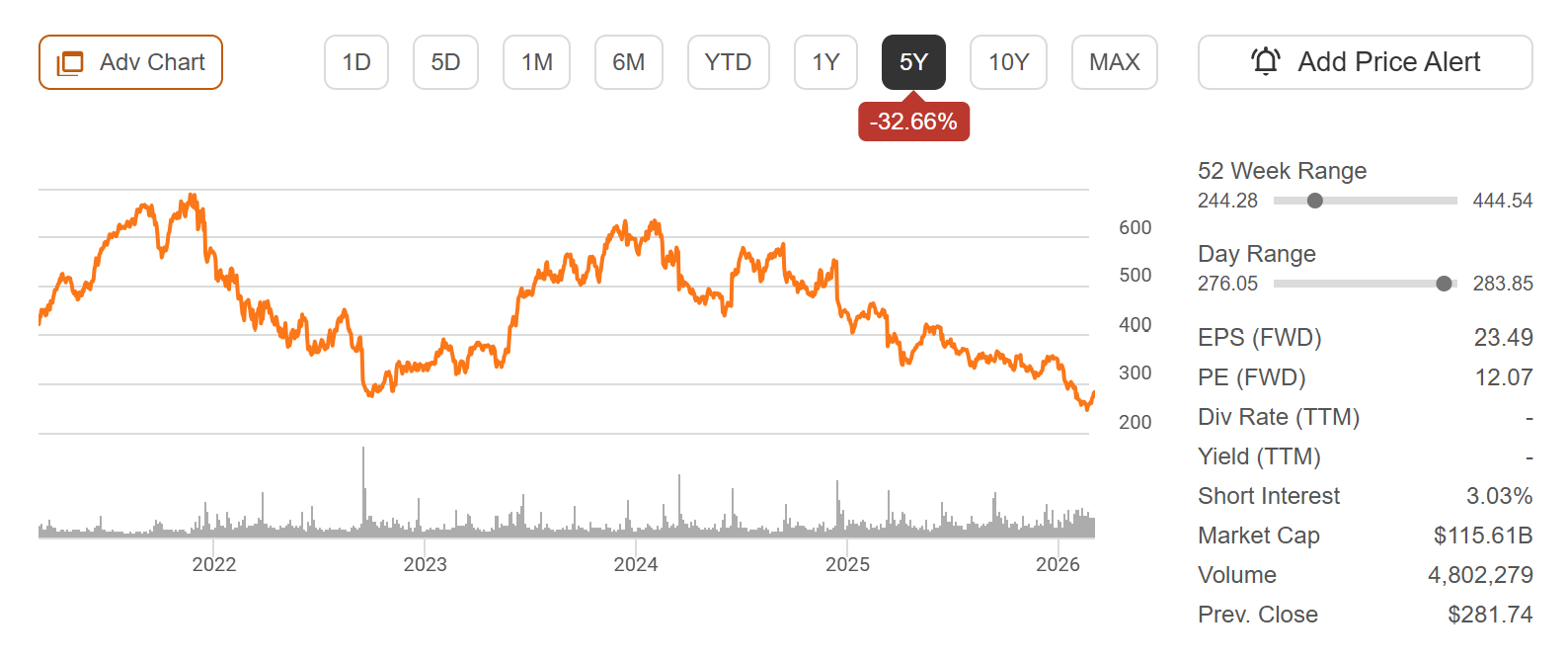

Adobe (ADBE)

Adobe (-18.9% YTD) reports Q1 FY2026 earnings this week, with investors focused on whether the company can convert its aggressive push into generative AI into sustained revenue growth — and stabilize sentiment after a volatile stretch for software stocks.

Last quarter, Adobe delivered record revenue of $6.19 billion (+10% YoY) and $5.50 in adjusted EPS, with strong demand across Creative Cloud, Acrobat, and AI-powered tools like Firefly helping drive engagement and subscription growth.

Heading into the release, investors will be watching three key themes:

Monetization of generative AI features, including Firefly and AI assistants

Digital Media ARR growth, a core indicator of subscription momentum

Enterprise demand for Experience Cloud, particularly marketing and analytics tools

Despite solid fundamentals, the stock has faced pressure as investors debate whether generative AI will strengthen Adobe’s ecosystem or disrupt traditional creative software pricing models, making this earnings report an important sentiment check for the broader software sector.

“We are leveraging AI to accelerate innovation and serve expanding audiences of creators and enterprises.”

Adobe, Inc. (ADBE) Stock Performance, 5-Year Chart, Seeking Alpha

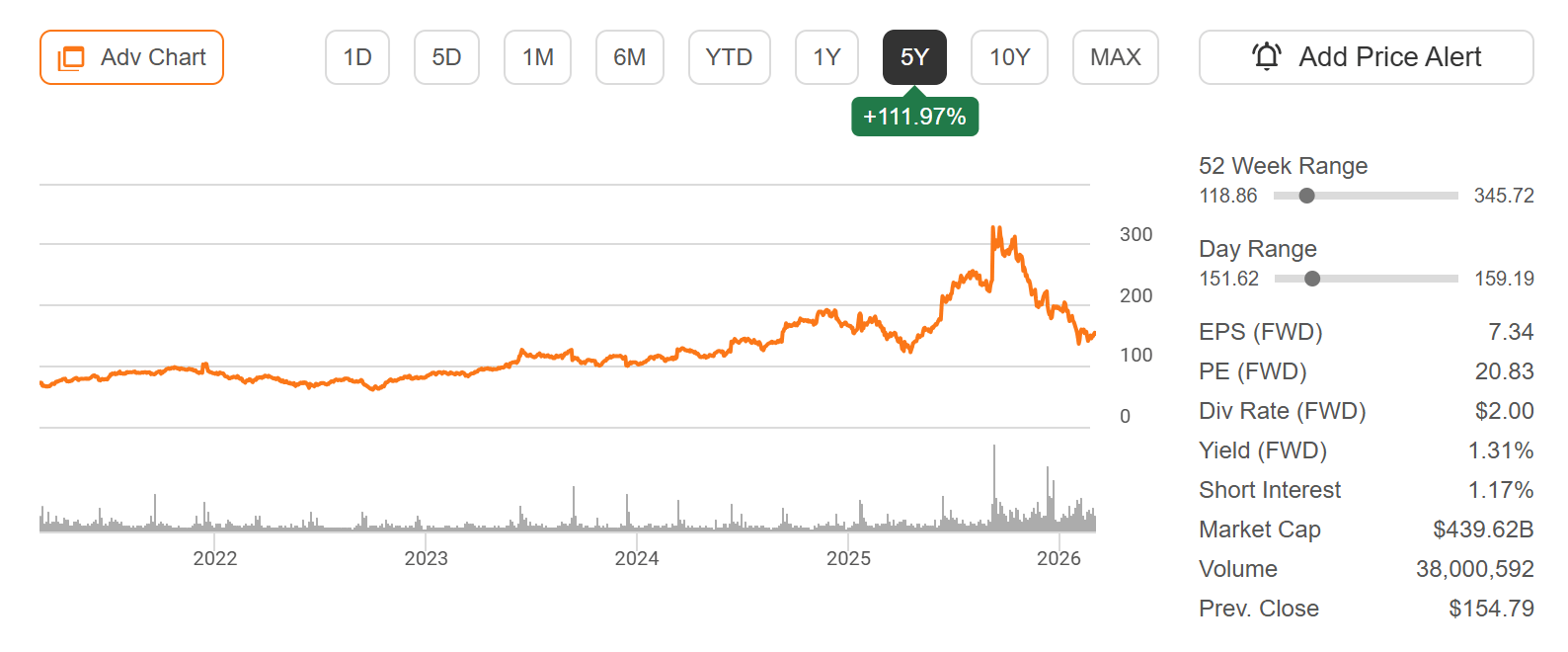

Oracle (ORCL)

Oracle (-21.5% YTD) reports Q3 FY2026 earnings this week, with investors focused on whether the company can maintain its rapid cloud-driven growth while funding one of the tech industry’s most aggressive AI infrastructure expansions.

Last quarter, Oracle delivered $16.1 billion in revenue (+14% YoY) and $2.26 in adjusted EPS, supported by strong cloud demand. Cloud revenue rose 34% to $8.0 billion, while Oracle Cloud Infrastructure (OCI) — a key platform for AI workloads – surged 68% year-over-year, driven by large enterprise and hyperscaler deployments.

Heading into the release, investors will be watching closely for:

OCI growth and AI-related cloud demand

Backlog conversion from massive contracted revenue commitments

Capital expenditure levels tied to AI data-center buildouts

Free-cash-flow pressure from infrastructure spending

Oracle has positioned itself as a major AI infrastructure provider alongside hyperscalers, but the market is increasingly focused on whether heavy spending today will translate into durable long-term margins and recurring cloud revenue.

“Remaining performance obligations surged as new commitments from major AI customers accelerated.”

Oracle Corporation (ORCL) Stock Performance, 5-Year Chart, Seeking Alpha

Investor Events / Global Affairs:

The energy markets will be closely watched as the Middle East conflict sends oil above $100/barrel.

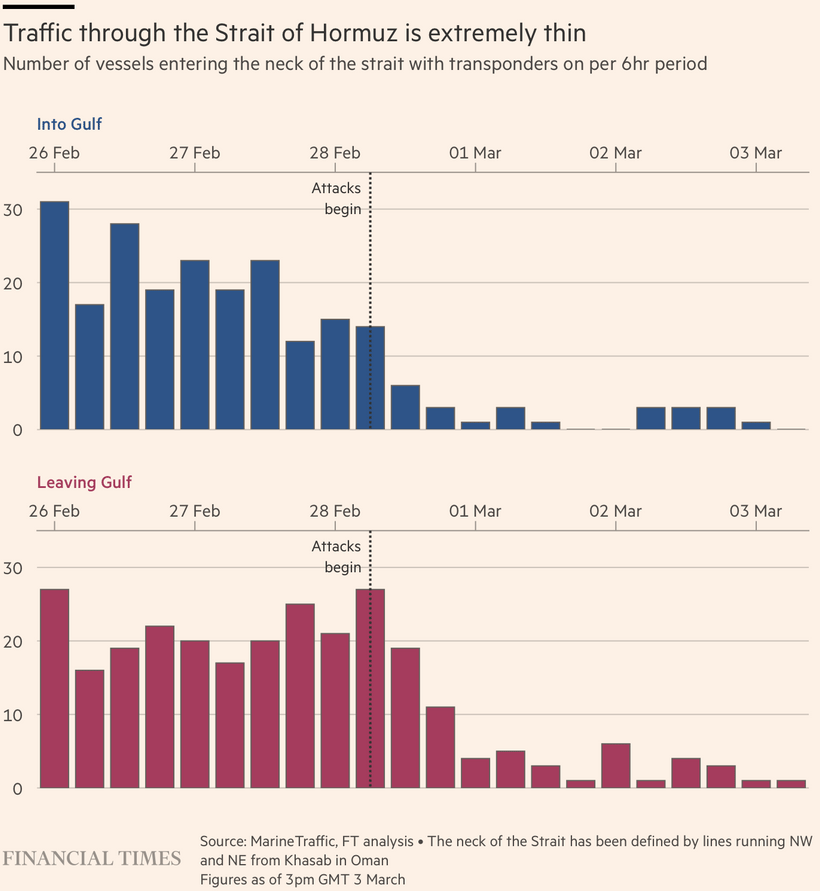

Middle East Conflict Sends Oil above $100 as Hormuz Traffic Halts

Oil markets will be closely watched this week after crude surged above $100 per barrel, with prices recently trading near $107, following escalating conflict in the Middle East and a near standstill in tanker traffic through the Strait of Hormuz.

Roughly 20 million barrels of oil per day — about one-fifth of global seaborne crude supply — normally flows through the strait, but shipping disruptions have reportedly stranded ~16 million barrels per day behind the chokepoint. The supply shock has triggered the fastest oil rally since the early stages of the Russia-Ukraine war in 2022.

Geopolitical tensions intensified after Donald Trump ordered diplomats to leave Saudi Arabia, while leadership changes in Iran and reports of Israeli strikes on Iranian fuel depots added to the uncertainty. The disruption has already begun filtering into consumer prices, with the average U.S. gasoline price rising 11% week-over-week to about $3.32 per gallon.

Markets reacted quickly to the geopolitical shock and weaker labor data, with major U.S. equity futures pulling lower to start the week. Investors will be watching closely for signs of whether tanker traffic resumes, how long supply remains constrained, and whether the spike in energy prices begins to feed back into inflation expectations and global growth forecasts.

“We are looking at what is by far the biggest disruption in world history in terms of daily oil production, if it goes on for weeks, it will reverberate across the global economy.”

Live Nation (LYV) Reaches Settlement in Federal Antitrust Case, Will Avoid Being Split Up

Sources: Hussein/Getty Images for Live Nation

The U.S. Department of Justice has reached a settlement with Live Nation that resolves its high-profile antitrust lawsuit against the concerts and ticketing giant, removing the possibility that the company would be broken up. Instead of forcing a structural separation between Live Nation and Ticketmaster, the agreement focuses on behavioral changes designed to boost competition.

Under the proposed deal, Live Nation would face restrictions on exclusive ticketing contracts and make it easier for rival promoters to compete for shows at venues the company controls. Roughly 10 states have agreed to the framework so far, though others — including New York — may continue pursuing separate legal action.

The lawsuit, originally filed in 2024, alleged that Live Nation illegally dominates the market for major concerts, harming artists, venues, and fans. Critics have long complained about the so-called “Ticketmaster tax,” with fees often adding 20% or more to ticket prices. For Live Nation, the settlement removes a major regulatory overhang and avoids the existential risk of a forced breakup. But the company will still face ongoing scrutiny from regulators and state attorneys general as competition in live entertainment continues to evolve.

Live Nation Entertainment, Inc. (LYV) Stock Performance, 5-Year Chart, Seeking Alpha

“In the lawsuit, Live Nation and Ticketmaster are accused of engaging in a variety of anticompetitive practices, including locking venues into long-term exclusive ticketing contracts and retaliating against rivals and venues that seek to use alternatives. The DOJ and states also say that Live Nation has monopolized the market for large, outdoor amphitheaters in the US.”

Major Economic Events:

A look at inflation readings and U.S. GDP.

Monday (3/9): None Scheduled

Tuesday (3/10): Existing Home Sales, NFIB Optimism Index

Wednesday (3/11): Existing Home Sales, NFIB Optimism Index

Thursday (3/12): Building Permits, Housing Starts, Initial Jobless Claims, U.S. Trade Deficit

Friday (3/13): Consumer Sentiment (Prelim), Core PCE Index, Core PCE Year Over Year, Durable Goods Orders, Durable Goods Orders ex-Transportation, GDP (First Revision), Job Openings (JOLTS), PCE Index, PCE Year Over Year, Personal Income, Personal Spending

What We’re Watching:

PCE Index

U.S. inflation slowed to 2.4% YoY in January, down from 2.7% in the prior two months and slightly below expectations of 2.5%. The drop marks the lowest annual inflation reading since May and reflects easing price pressures across several key categories.

Energy played a major role in the slowdown, with prices falling 0.1% after rising 2.3% in December. Gasoline prices declined sharply (-7.5%), while fuel oil also dropped (-4.2%), helping offset still-elevated natural gas costs. Inflation also cooled in used vehicles (-2%), while price increases moderated slightly in food and shelter.

On a monthly basis, headline CPI rose 0.2%, below expectations for a 0.3% increase. Core inflation, which excludes food and energy, eased to 2.5% YoY – its lowest level since March 2021.

Economists expect the following this week:

CPI (YoY): 2.4% vs. 2.7% prior

Core CPI (YoY): 2.5% vs. 2.6% prior

CPI (MoM): 0.2% vs. 0.3% prior

“Even a modest data center boom could substantially raise retail electricity prices and hence annual inflation. For example, under plausible assumptions about the data center build-out and utilization, annual PCE inflation in 2030 would increase by between 0.04 and 0.13 percentage points. Slower-than-expected growth of renewable energy sources—wind and solar—could nearly double the inflationary effect.”

U.S. GDP

The U.S. economy grew at an annualized 1.4% in Q4 2025, well below expectations of 3% and down sharply from 4.4% growth in Q3, marking the slowest expansion since early 2025. The deceleration was driven primarily by softer consumer spending and a sharp contraction in government outlays tied to the recent government shutdown.

Consumer spending — the backbone of the U.S. economy — slowed to 2.4% from 3.5%, with goods purchases slipping slightly while services spending remained solid at 3.4%. Trade also turned into a modest drag, with exports falling 0.9% after a surge the previous quarter.

The biggest headwind came from government spending and investment, which dropped 5.1%, subtracting nearly 0.9 percentage points from overall GDP. On the more positive side, business investment strengthened.

For the full year, the U.S. economy grew 2.2% in 2025, slowing from 2.8% in 2024. This week — we’ll be seeing the first revision to Q4 2025 GDP numbers — which are expected to show slightly lower growth.

Economists expect the following this week:

Q4 GDP (QoQ Annualized): +1.4% vs. +4.4% prior

Consumer Spending: +2.4% vs. +3.5% prior

Government Spending: -5.1% vs. +2.2% prior

“Paul Ashworth, chief North America economist at Capital Economics, said in a note following the release that the shutdown was a larger-than-expected drag during the fourth quarter, but he expects this impact to be reversed in the first quarter of 2026, when his firm forecasts annualized GDP growth will hit 3%.”

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

This content is sponsored by NEOS Investments. The creator is compensated by NEOS to discuss NEOS ETFs. This content is for informational purposes only, and is not personalized investment, tax, or legal advice, and does not constitute an offer to buy or sell any security. Investing involves risk, including possible loss of principal. Before investing, carefully review the NEOS ETFs prospectus at neosfunds.com.

Grit is a publisher of financial information, not an investment advisor. Grit does not provide personalized or individualized investment advice or information that is tailored to the needs of any particular recipient. Grit does not guarantee the accuracy or completeness of the information provided in this page. All statements and expressions herein are the sole opinion of the author or paid advertiser.

Cover Image Source: FX Empire

THE INFORMATION CONTAINED ON THIS WEBSITE IS NOT AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE, AND DOES NOT PURPORT TO BE AND DOES NOT EXPRESS ANY OPINION AS TO THE PRICE AT WHICH THE SECURITIES OF ANY COMPANY MAY TRADE AT ANY TIME. THE INFORMATION AND OPINIONS PROVIDED HEREIN SHOULD NOT BE TAKEN AS SPECIFIC ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. INVESTORS SHOULD MAKE THEIR OWN INVESTIGATION AND DECISIONS REGARDING THE PROSPECTS OF ANY COMPANY DISCUSSED HEREIN BASED ON SUCH INVESTORS’ OWN REVIEW OF PUBLICLY AVAILABLE INFORMATION AND SHOULD NOT RELY ON THE INFORMATION CONTAINED HEREIN. INVESTORS SHOULD OBTAIN INDIVIDUAL INVESTMENT ADVICE BASED ON THEIR OWN CIRCUMSTANCES BEFORE MAKING AN INVESTMENT DECISION

No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer or the solicitation of an offer to buy or sell the securities or financial instruments mentioned.

The author, publisher or insiders of the publisher may currently have long or short positions in the securities of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Any projections, market outlooks or estimates herein are forward looking statements and are inherently unreliable. They are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities discussed herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and Grit undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional material.

Grit does not accept any liability whatsoever for any direct or consequential loss, however arising, directly or indirectly, from any use of the information contained herein.

By using the Site or any related social media account, you are indicating your consent and agreement to this disclaimer and our terms of use. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Please read: Terms of Use, Privacy Policy, Disclosure Policy and Disclaimer Policy

If you have any questions please contact us at [email protected]